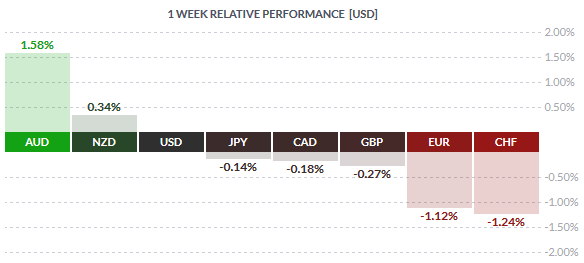

The Aussie dollar closed the week with 1.58% in gains against the Greenback marking a second straight week of rally. Prices touched a 5-week low previously before reversing off the lows. With the weekly prices forming a bullish engulfing previously the Aussie could potentially rally higher in the near term. The Kiwi dollar was the second best performing currency despite a few setbacks with the GDT posting another week of falling prices.

The Euro remained extremely bearish last week as Mario Draghi’s dovish comments on further easing in December sent the Euro down -1.12% lower. The market expectations are pricing in further additional QE in December along with rate cuts to the deposit rates which are already in negative territory.

Fundamentals for the Week 23/11 – 27/11

| Date | Time | Currency | Detail | Forecast | Previous |

| 23-Nov | 10:00 | EUR | French Flash Manufacturing PMI | 50.6 | 50.6 |

| EUR | French Flash Services PMI | 52.1 | 52.7 | ||

| 10:30 | EUR | German Flash Manufacturing PMI | 52.2 | 52.1 | |

| EUR | German Flash Services PMI | 54.3 | 54.5 | ||

| 11:00 | EUR | Flash Manufacturing PMI | 52.3 | 52.3 | |

| EUR | Flash Services PMI | 54.2 | 54.1 | ||

| 16:45 | USD | Flash Manufacturing PMI | 54 | 54.1 | |

| 17:00 | USD | Existing Home Sales | 5.41M | 5.55M | |

| Tentative | USD | Fed Announcement | |||

| 24-Nov | 03:35 | JPY | Flash Manufacturing PMI | 52.1 | 52.4 |

| 09:00 | EUR | German Final GDP q/q | 0.30% | 0.30% | |

| 10:15 | CHF | Employment Level | |||

| 11:00 | EUR | German Ifo Business Climate | 108.3 | 108.2 | |

| 11:05 | AUD | RBA Gov Stevens Speaks | |||

| 13:00 | GBP | CBI Realized Sales | 25 | 19 | |

| 15:30 | USD | Prelim GDP q/q | 2.00% | 1.50% | |

| USD | Goods Trade Balance | -61.8B | -58.6B | ||

| USD | Prelim GDP Price Index q/q | 1.20% | 1.20% | ||

| USD | S&P/CS Composite-20 HPI y/y | 5.20% | 5.10% | ||

| 17:00 | USD | CB Consumer Confidence | 99.3 | 97.6 | |

| USD | Richmond Manufacturing Index | 0 | -1 | ||

| 22:30 | CAD | Gov Council Member Patterson Speaks | |||

| 25-Nov | 01:50 | JPY | Monetary Policy Meeting Minutes | ||

| JPY | SPPI y/y | 0.60% | 0.60% | ||

| 02:30 | AUD | Construction Work Done q/q | -1.80% | 1.60% | |

| 11:30 | GBP | BBA Mortgage Approvals | 45.5K | 44.5K | |

| 12:00 | EUR | Italian Retail Sales m/m | 0.50% | 0.30% | |

| 12:20 | AUD | RBA Assist Gov Debelle Speaks | |||

| 14:30 | GBP | Autumn Forecast Statement | |||

| 15:30 | USD | Core Durable Goods Orders m/m | 0.50% | -0.30% | |

| USD | Unemployment Claims | 273K | 271K | ||

| USD | Core PCE Price Index m/m | 0.10% | 0.10% | ||

| USD | Durable Goods Orders m/m | 1.60% | -1.20% | ||

| USD | Personal Spending m/m | 0.30% | 0.10% | ||

| USD | Personal Income m/m | 0.40% | 0.10% | ||

| 16:00 | USD | HPI m/m | 0.50% | 0.30% | |

| 16:45 | USD | Flash Services PMI | 55.2 | 54.8 | |

| 17:00 | USD | New Home Sales | 500K | 468K | |

| USD | Revised UoM Consumer Sentiment | 93.2 | 93.1 | ||

| USD | Revised UoM Inflation Expectations | 2.50% | |||

| 17:30 | USD | Crude Oil Inventories | 0.3M | ||

| 23:45 | NZD | Trade Balance | -1000M | -1222M | |

| 26-Nov | 02:30 | AUD | Private Capital Expenditure q/q | -2.80% | -4.00% |

| 11:00 | EUR | M3 Money Supply y/y | 4.90% | 4.90% | |

| EUR | Private Loans y/y | 1.20% | 1.10% | ||

| 14:00 | EUR | GfK German Consumer Climate | 9.2 | 9.4 | |

| 15:30 | CAD | Corporate Profits q/q | 12.90% | ||

| 27-Nov | 01:30 | JPY | Household Spending y/y | 0.00% | -0.40% |

| JPY | Tokyo Core CPI y/y | -0.10% | -0.20% | ||

| JPY | National Core CPI y/y | -0.10% | -0.10% | ||

| JPY | Unemployment Rate | 3.40% | 3.40% | ||

| 02:05 | GBP | GfK Consumer Confidence | 2 | 2 | |

| 09:00 | EUR | German Import Prices m/m | -0.10% | -0.70% | |

| 27th-30th | GBP | Nationwide HPI m/m | 0.60% | ||

| 09:45 | EUR | French Consumer Spending m/m | 0.20% | 0.00% | |

| 10:00 | EUR | Spanish Flash CPI y/y | -0.50% | -0.70% | |

| 11:30 | GBP | Second Estimate GDP q/q | 0.50% | 0.50% | |

| GBP | Prelim Business Investment q/q | 1.50% | 1.60% | ||

| GBP | Index of Services 3m/3m | 0.80% | 0.90% | ||

| Tentative | EUR | ECB Financial Stability Review | |||

| 15:30 | CAD | RMPI m/m | 3.00% | ||

| CAD | IPPI m/m | -0.30% |

Time: GMT+2

Currencies/Events to Watch this Week

AUD: It is a slow week for the Australian dollar with lack of any major news to go by. Data this coming week includes the Private capital expenditure for the quarter which is expected to decline -2.8%, while construction work done for the quarter is expected to fall -1.8%. Besides these two main economic events, RBA Governor Stevens is scheduled to speak earlier in the week. With strong gains posted by the Aussie last week, the currency could pause its rally this week and could remain susceptible to the US Dollar strength or weakness.

CAD: There are no major economic events scheduled for the Canadian dollar this week and the currency is likely to be trading off the US Dollar’s fundamental risk events. Oil prices could also be highlighted over the week on lack of any major events that are due.

EUR: It will be a busy week for the Eurozone with various flash manufacturing and services PMI numbers due from the region. German GDP numbers are expected to show a quarterly growth of 0.3%, unchanged from the previous quarterly growth. The week ends with the ECB releasing the financial stability report. With most of the ECB speeches done with the Euro is likely to take a breather in the near term.

GBP: Data from the UK this week will see the second estimates of the third quarter GDP. Expectations are for an unchanged GDP print at 0.5%. The British Pound has managed to recover off the declines from the previous weeks and the GDP numbers, on lack of any other major economic data could be the main risk event.

JPY: Data from Japan will see the monetary policy meeting minutes being released. With the BoJ standing pat on policy, the minutes are unlikely to being any big volatility in the markets. Other data from Japan includes the unemployment rate and consumer inflation numbers on a short trading week with the Japanese markets closed on Monday.

USD: The week ahead from the US will be a busy one with the second revision to the quarterly GDP. Expectations are bullish, calling for a 2.0% increase, up from 1.5% from the first estimates. A rise in the third quarter GDP could potentially boost the Greenback in the near term. Other main events during the week includes the Fed announcement and the durable goods orders data which is expected to rebound 0.5%, after declining -0.3% previously. The US markets are closed on Thursday the 26th November on account of Thanksgiving.