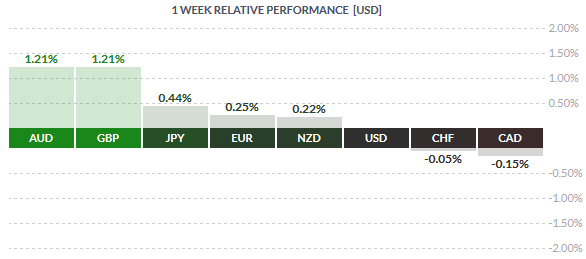

The Australian Dollar emerged on tops last week as the currency gained nearly 1.21% against the Greenback. The gains in the Aussie came as the economy posted a strong jobs report which saw the unemployment rate decline sharply from 6.2% to 5.9% allaying speculation of any further rate cuts from the RBA. The Aussie’s gains come after nearly 4-weeks of consecutive declines which saw the currency decline off the highs near 0.726 in early September.

The US Dollar gave back some of its gains despite a hawkish narrative from the Fed members. Economic data was however mixed last week as the retail sales and Producer prices index posted weak numbers. The Euro managed to make modest gains by late Friday, rising 0.25% to the Greenback. The Swiss Franc and the Canadian dollar were the weakest currencies for the week, losing -005% and -0.15% respectively.

Fundamentals for the Week 16/11 – 20/11

| Date | Time | Currency | Detail | Forecast | Previous |

| 16-Nov | 01:50 | JPY | Prelim GDP q/q | -0.10% | -0.30% |

| JPY | Prelim GDP Price Index y/y | 1.70% | 1.50% | ||

| 02:01 | GBP | Rightmove HPI m/m | 0.60% | ||

| 02:30 | AUD | New Motor Vehicle Sales m/m | 5.50% | ||

| 12:00 | EUR | Final CPI y/y | 0.00% | 0.00% | |

| EUR | Final Core CPI y/y | 1.00% | 1.00% | ||

| 12:15 | EUR | ECB President Draghi Speaks | |||

| 15:30 | CAD | Manufacturing Sales m/m | 0.30% | -0.20% | |

| CAD | Foreign Securities Purchases | 4.12B | 3.11B | ||

| USD | Empire State Manufacturing Index | -5.3 | -11.4 | ||

| 23:30 | AUD | RBA Assist Gov Kent Speaks | |||

| 17-Nov | 02:30 | AUD | Monetary Policy Meeting Minutes | ||

| 04:00 | NZD | Inflation Expectations q/q | 1.90% | ||

| 11:00 | EUR | Italian Trade Balance | 2.24B | 1.85B | |

| 11:30 | GBP | CPI y/y | -0.10% | -0.10% | |

| GBP | PPI Input m/m | 0.20% | 0.60% | ||

| GBP | RPI y/y | 0.90% | 0.80% | ||

| GBP | Core CPI y/y | 1.00% | 1.00% | ||

| GBP | HPI y/y | 5.40% | 5.20% | ||

| GBP | PPI Output m/m | -0.10% | -0.10% | ||

| 12:00 | EUR | German ZEW Economic Sentiment | 6.7 | 1.9 | |

| EUR | ZEW Economic Sentiment | 35.2 | 30.1 | ||

| 15:30 | USD | CPI m/m | 0.20% | -0.20% | |

| USD | Core CPI m/m | 0.20% | 0.20% | ||

| 16:15 | USD | Capacity Utilization Rate | 77.50% | 77.50% | |

| USD | Industrial Production m/m | 0.10% | -0.20% | ||

| Tentative | NZD | GDT Price Index | -7.40% | ||

| 17th-19th | USD | Mortgage Delinquencies | 5.30% | ||

| 17:00 | USD | NAHB Housing Market Index | 64 | 64 | |

| 18-Nov | 00:15 | AUD | RBA Assist Gov Debelle Speaks | ||

| 01:00 | AUD | CB Leading Index m/m | -0.40% | ||

| 01:30 | AUD | MI Leading Index m/m | 0.10% | ||

| 02:30 | AUD | Wage Price Index q/q | 0.60% | 0.60% | |

| 12:00 | CHF | ZEW Economic Expectations | 18.3 | ||

| 15:00 | USD | FOMC Member Lockhart Speaks | |||

| 15:30 | USD | Building Permits | 1.15M | 1.11M | |

| USD | Housing Starts | 1.16M | 1.21M | ||

| 17:30 | USD | Crude Oil Inventories | 4.2M | ||

| 21:00 | USD | FOMC Meeting Minutes | |||

| 23:45 | NZD | PPI Input q/q | -0.30% | ||

| NZD | PPI Output q/q | -0.20% | |||

| 19-Nov | 01:50 | JPY | Trade Balance | -0.38T | -0.36T |

| Tentative | JPY | Monetary Policy Statement | |||

| 06:30 | JPY | All Industries Activity m/m | 0.20% | -0.20% | |

| Tentative | JPY | BOJ Press Conference | |||

| 09:00 | CHF | Trade Balance | 3.18B | 3.05B | |

| 10:00 | EUR | German Buba President Weidmann Speaks | |||

| 11:00 | EUR | Current Account | 18.3B | 17.7B | |

| 11:30 | GBP | Retail Sales m/m | -0.40% | 1.90% | |

| 13:00 | GBP | CBI Industrial Order Expectations | -10 | -18 | |

| 14:30 | EUR | ECB Monetary Policy Meeting Accounts | |||

| 15:30 | CAD | Wholesale Sales m/m | -0.10% | ||

| USD | Unemployment Claims | 272K | 276K | ||

| 17:00 | USD | Philly Fed Manufacturing Index | 0.1 | -4.5 | |

| USD | CB Leading Index m/m | 0.50% | -0.20% | ||

| 17:30 | USD | Natural Gas Storage | |||

| 19:30 | CHF | Gov Board Member Maechler Speaks | |||

| USD | FOMC Member Lockhart Speaks | ||||

| 20-Nov | 04:00 | CNY | CB Leading Index m/m | 1.60% | |

| 07:00 | JPY | BOJ Monthly Report | |||

| 09:00 | EUR | German PPI m/m | -0.20% | -0.40% | |

| 10:00 | EUR | ECB President Draghi Speaks | |||

| 11:30 | GBP | Public Sector Net Borrowing | 5.5B | 8.6B | |

| 12:15 | EUR | German Buba President Weidmann Speaks | |||

| 15:30 | CAD | Core CPI m/m | 0.20% | ||

| CAD | Core Retail Sales m/m | 0.00% | |||

| CAD | CPI m/m | -0.20% | |||

| CAD | Retail Sales m/m | 0.50% | |||

| 17:00 | EUR | Consumer Confidence | -7 | -8 |

Time: GMT+2

Currencies/Events to Watch this Week

RBA Monetary Policy Minutes: The RBA’s meeting minutes from the monetary policy meeting conducted earlier this month will be due for release on 17th November. Not much is expected from the minutes and if there are any signs of dovishness, the markets are most likely to ignore the minutes considering the strong jobs report seen last week. The Aussie dollar is likely to keep a bullish front into the week ahead on lack of any major market data.

Canada Inflation: Consumer inflation data from Canada is due next week followed by retail sales being released simultaneously. Inflation was steady at 0.2% last month on the core while the headline CPI fell -0.2%. A potential surprise to the upside could see some relief recovery in USDCAD which has been trending strongly. Ahead of the inflation and retail sales data which is due on 20th November, manufacturing sales is due for release on 16th November. Expectations are for retail sales to have risen 0.3% for the month after declining -0.2% previously

Eurozone Inflation: Inflation data from Eurozone will be the main event risk next week due for release on 16th November. Expectations remain subdued on both the core and the headline CPI which is likely to keep pressure on the Euro. ECB President Draghi is due to speak later on Monday and any dovish talk on QE will likely see the Euro remaining well sold across the board. Data for the remainder of the week is quiet with the exception of another speech by Mario Draghi due on November 20th.

UK Inflation: After enjoying a strong week, recovering off the previous week’s dovish inflation forecasts, the week ahead for the UK will see the inflation numbers being released on 17th November. Expectations are dovish with the headline CPI estimated to fall -0.1%, while the core CPI is expected to stay unchanged at 1.0%. Retail sales numbers are also due later in the week on November 19th with expectations of a decline of -0.4% after retail sales increased 1.9% a month ago.

Japan GDP: The quarterly GDP numbers from Japan will be the main event risk early Monday morning on November 16th. Expectations are for the Japanese GDP to have contracted -0.1%, after initial estimates saw a -0.3% contraction. A better than expected GDP numbers is likely to help support the Yen in the near term. However, the main event next week is the Bank of Japan press conference and monetary policy. No major changes are expected at this meeting.

New Zealand inflation expectations: Quarterly inflation expectations data is due for release on 17th November which currently stands at 1.9%. Global dairy trade data is also due for release later in the day. Prices fell -7.4% previously and a continued decline will keep the Kiwi subdued. Producer Price index data is due on 18th November and the expectations are dovish after PPI fell -0.3% previously.

US Inflation and FOMC Meeting minutes: Consumer inflation data in the US is due for release on the 17th November with market expectations of 0.2% increase on both the headline and the core after inflation was mixed previously. A beat on the estimates could keep the Dollar well supported and would cement the Fed’s view for a rate hike in December. The most important event for the week ahead however will be the FOMC meeting minutes due for release on 18th November. Expectations are for the meeting minutes to paint a hawkish picture, in line with the hawkish statement released in October.