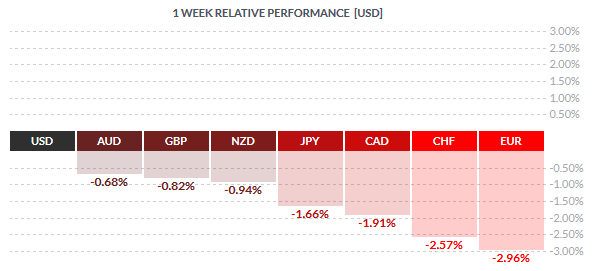

The US Dollar managed to emerge on the top last week led by steep losses in the Euro, which closed the week -2.96% lower. The ECB’s willingness to expand its QE program led the Euro to drop in anticipation of further QE to be announced in the December ECB meeting. The Swiss Franc was the second weakest currency losing -2.57%. The Bank of Canada also met last week where interest rates were unchanged. But with the BoC striking a dovish tone, the Canadian dollar closed the week with -1.91% losses.

The commodity risk currencies were seen to be faring better this week despite the Australian dollar declining -0.68% to the Greenback but fared better against its peers. The New Zealand Dollar which was in a strong short term rally was showing signs of weakness as the currency fell -0.94% ahead of the RBNZ’s interest rate decision this week.

Fundamentals for the Week 26/10 – 30/10

| Date | Time | Currency | Detail | Forecast | Previous |

| 26-Oct | 12:00 | EUR | German Ifo Business Climate | 108.1 | 108.5 |

| 12:30 | GBP | BBA Mortgage Approvals | 46.2K | 46.7K | |

| 14:00 | GBP | CBI Industrial Order Expectations | -8 | -7 | |

| Tentative | EUR | German Buba Monthly Report | |||

| 17:00 | USD | New Home Sales | 546K | 552K | |

| 27-Oct | 00:45 | NZD | Trade Balance | -822M | -1035M |

| 02:50 | JPY | SPPI y/y | 0.60% | 0.70% | |

| 10:00 | CHF | UBS Consumption Indicator | 1.63 | ||

| 12:00 | EUR | M3 Money Supply y/y | 5.00% | 4.80% | |

| EUR | Private Loans y/y | 1.10% | 1.00% | ||

| 12:30 | GBP | Prelim GDP q/q | 0.60% | 0.70% | |

| GBP | Index of Services 3m/3m | 1.00% | 0.80% | ||

| Tentative | GBP | 10-y Bond Auction | 1.95|1.4 | ||

| 15:30 | USD | Core Durable Goods Orders m/m | 0.00% | -0.20% | |

| USD | Durable Goods Orders m/m | -1.10% | -2.30% | ||

| 16:00 | USD | S&P/CS Composite-20 HPI y/y | 5.10% | 5.00% | |

| 16:45 | USD | Flash Services PMI | 55.3 | 55.1 | |

| 17:00 | USD | CB Consumer Confidence | 102.5 | 103 | |

| USD | Richmond Manufacturing Index | -3 | -5 | ||

| 18:20 | CAD | Gov Council Member Lane Speaks | |||

| 28-Oct | 02:50 | JPY | Retail Sales y/y | 0.50% | 0.80% |

| 03:30 | AUD | CPI q/q | 0.70% | 0.70% | |

| AUD | Trimmed Mean CPI q/q | 0.50% | 0.60% | ||

| 10:00 | EUR | German Import Prices m/m | -0.20% | -1.50% | |

| EUR | GfK German Consumer Climate | 9.5 | 9.6 | ||

| Tentative | EUR | German 10-y Bond Auction | 0.62|1.1 | ||

| 15:30 | USD | Goods Trade Balance | -64.9B | -67.2B | |

| 17:30 | USD | Crude Oil Inventories | 8.0M | ||

| 21:00 | USD | FOMC Statement | |||

| USD | Federal Funds Rate | <0.25% | <0.25% | ||

| 23:00 | NZD | Official Cash Rate | 2.75% | 2.75% | |

| NZD | RBNZ Rate Statement | ||||

| 29-Oct | 02:50 | JPY | Prelim Industrial Production m/m | -0.50% | -1.20% |

| 03:00 | AUD | HIA New Home Sales m/m | 2.30% | ||

| 03:30 | AUD | Import Prices q/q | 1.60% | 1.40% | |

| 10:00 | GBP | Nationwide HPI m/m | 0.50% | 0.50% | |

| All Day | EUR | German Prelim CPI m/m | -0.10% | -0.20% | |

| 11:00 | EUR | Spanish Flash CPI y/y | -0.60% | -0.90% | |

| 11:55 | EUR | German Unemployment Change | -4K | 2K | |

| 12:30 | GBP | Net Lending to Individuals m/m | 4.4B | 4.3B | |

| GBP | M4 Money Supply m/m | -0.20% | -0.40% | ||

| GBP | Mortgage Approvals | 73K | 71K | ||

| 14:00 | GBP | CBI Realized Sales | 35 | 49 | |

| 15:30 | CAD | RMPI m/m | -6.60% | ||

| CAD | IPPI m/m | -0.30% | |||

| USD | Advance GDP q/q | 1.60% | 3.90% | ||

| USD | Unemployment Claims | 264K | 259K | ||

| USD | Advance GDP Price Index q/q | 1.50% | 2.10% | ||

| 16:10 | USD | FOMC Member Lockhart Speaks | |||

| 17:00 | USD | Pending Home Sales m/m | 1.10% | -1.40% | |

| 30-Oct | 00:45 | NZD | Building Consents m/m | -4.90% | |

| 02:30 | JPY | Household Spending y/y | 1.20% | 2.90% | |

| JPY | Tokyo Core CPI y/y | -0.20% | -0.20% | ||

| JPY | National Core CPI y/y | -0.20% | -0.10% | ||

| JPY | Unemployment Rate | 3.40% | 3.40% | ||

| 03:00 | NZD | ANZ Business Confidence | -18.9 | ||

| 03:05 | GBP | GfK Consumer Confidence | 4 | 3 | |

| 03:30 | AUD | PPI q/q | 0.30% | ||

| AUD | Private Sector Credit m/m | 0.50% | 0.60% | ||

| Tentative | JPY | Monetary Policy Statement | |||

| 08:00 | JPY | Housing Starts y/y | 6.50% | 8.80% | |

| 09:00 | JPY | BOJ Outlook Report | |||

| Tentative | JPY | BOJ Press Conference | |||

| 10:00 | EUR | German Retail Sales m/m | 0.40% | -0.40% | |

| 10:45 | EUR | French Consumer Spending m/m | 0.20% | 0.00% | |

| 11:00 | CHF | KOF Economic Barometer | 100.1 | 100.4 | |

| EUR | Spanish Flash GDP q/q | 0.90% | 1.00% | ||

| 12:00 | EUR | Italian Monthly Unemployment Rate | 11.90% | 11.90% | |

| 13:00 | EUR | CPI Flash Estimate y/y | 0.00% | -0.10% | |

| EUR | Core CPI Flash Estimate y/y | 0.90% | 0.90% | ||

| EUR | Unemployment Rate | 11.00% | 11.00% | ||

| EUR | Italian Prelim CPI m/m | 0.10% | -0.40% | ||

| 15:30 | CAD | GDP m/m | 0.10% | 0.30% | |

| USD | Employment Cost Index q/q | 0.60% | 0.20% | ||

| USD | Core PCE Price Index m/m | 0.20% | 0.10% | ||

| USD | Personal Spending m/m | 0.20% | 0.40% | ||

| USD | Personal Income m/m | 0.20% | 0.30% | ||

| 16:45 | USD | Chicago PMI | 49.5 | 48.7 | |

| 17:00 | USD | FOMC Member Williams Speaks | |||

| USD | Revised UoM Consumer Sentiment | 92.6 | 92.1 | ||

| USD | Revised UoM Inflation Expectations | 2.70% |

Time: GMT+3

Currencies/Events to Watch this Week

Australia Inflation: Quarterly inflation numbers are due from Australia this week. On 28th October, the quarterly CPI and trimmed mean CPI futures are due out. Expectations are for the inflation to have remained steady at 0.7% while the trimmed mean CPI is expected to post a soft decline, rising 0.5% from 0.6% previously. The producer price index is also due out with the previous quarter posting 0.3% growth, down from 0.5% previously. The Australian dollar has remained weak for two straight weeks after posting a strong rally the previous two weeks. A break above the previous higher close of 0.7328 is needed for further gains.

Canada GDP: Canadian monthly GDP numbers are due out this week with expectations of a soft reading of 0.1% for the month of September, down from 0.3% previously. It is essential for the Canadian GDP to beat estimates and stay in the positive after GDP for the months of April through June remained in negative territory but started to decline since July which saw a strong increase in GDP to 0.5%.

Busy week for the Euro: The week ahead will see a lot of economic releases from the Eurozone, the most important being the German Ifo business climate which is forecasted to have fallen to 108.1 from 108.5 previously. The week will also see flash and preliminary CPI estimates, one that could take importance in light of Draghi’s recent comments at the ECB meeting last week. A continued weak inflation figures is likely to keep the Euro subdued on hopes of QE expansion in December

UK Preliminary GDP: The third quarter GDP estimates is due this week and expectations are for the UK GDP to have risen at a slower pace of 0.6%, down from 0.7% during the second quarter. However, there is a scope for a miss on the estimates given the relatively weaker performance during the third quarter in the UK. Besides the GDP estimates, there are no other major releases pertaining to the UK

BoJ Monetary Policy: The Bank of Japan will meet this week for its monetary policy review. Expectations are divided with some institutions hoping to see the Bank of Japan increase its stimulus purchase program. However, it could be a tricky meeting considering that until recently, BoJ Governor Kuroda maintained that inflation is expected to meet the Central Bank’s target by fiscal year of 2017.

RBNZ Policy meeting: The Reserve Bank of New Zealand’s monetary policy decision is due on 28th October with expectations that the RBNZ could hold interest rates steady at 2.75%. An unchanged interest rate decision could see the Kiwi keep its gains. The NZDUSD has gained for three straight weeks so far with last week closing in the negative.

FOMC and US GDP: It will be a very important week for the US Dollar as the durable goods orders are due followed by the FOMC monetary policy statement. Expectations are for the Federal Reserve to leave policy unchanged in light of weak economic data and the global economic slowdown. A day later, the advance GDP estimates are due with expectations that the US economy grew at a much subdued pace of 1.6% after rising 3.9% previously.