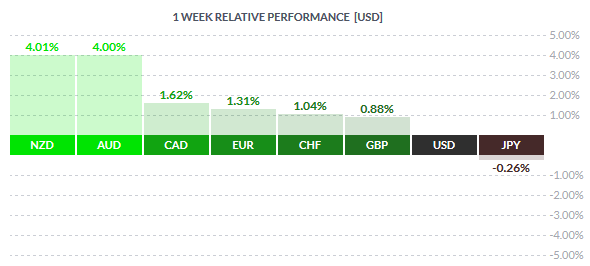

The commodity risk currencies, the Aussie, Kiwi and the Canadian dollar saw sharp gains this week, rising on average of 4.0% in what seems to be a risk on sentiment. The weak US Dollar led by dovish FOMC minutes saw the markets sell the Greenback in favor of riskier currencies. The US Dollar was the weakest, second to the Japanese Yen which declined -0.26% for the week.

With the consensus expecting to see the US Federal Reserve leaves rates unchanged in October, it is likely that the Greenback could post further declines in the week ahead. The most important data however will be the US inflation numbers and retail sales which could bring volatility to the markets.

Fundamentals for the Week 12/10 – 17/10

| Date | Time | Currency | Detail | Forecast | Previous |

| 12-Oct | 15:10 | USD | FOMC Member Lockhart Speaks | ||

| 16:30 | GBP | CB Leading Index m/m | -0.30% | ||

| 17:30 | USD | FOMC Member Evans Speaks | |||

| 20:20 | CAD | BOC Gov Poloz Speaks | |||

| 23:30 | USD | FOMC Member Brainard Speaks | |||

| 13-Oct | 00:40 | AUD | RBA Deputy Gov Lowe Speaks | ||

| 00:45 | NZD | FPI m/m | -0.50% | ||

| 02:01 | GBP | BRC Retail Sales Monitor y/y | -1.00% | ||

| 02:50 | JPY | Monetary Policy Meeting Minutes | |||

| JPY | Bank Lending y/y | 2.70% | |||

| 03:30 | AUD | NAB Business Confidence | 1 | ||

| 13th-17th | CNY | Foreign Direct Investment ytd/y | 9.20% | ||

| Tentative | CNY | Trade Balance | 47.8B | 60.2B | |

| 08:00 | JPY | Consumer Confidence | 41.6 | 41.7 | |

| 09:00 | EUR | German Final CPI m/m | -0.20% | -0.20% | |

| EUR | German WPI m/m | -0.30% | -0.80% | ||

| JPY | Prelim Machine Tool Orders y/y | -16.50% | |||

| 10:15 | CHF | PPI m/m | -0.10% | -0.70% | |

| 13th-14th | CNY | M2 Money Supply y/y | 13.10% | 13.30% | |

| 13th-14th | CNY | New Loans | 900B | 810B | |

| 11:30 | GBP | CPI y/y | 0.00% | 0.00% | |

| GBP | BOE Credit Conditions Survey | ||||

| GBP | PPI Input m/m | 0.20% | -2.40% | ||

| GBP | RPI y/y | 1.00% | 1.10% | ||

| GBP | Core CPI y/y | 1.10% | 1.00% | ||

| GBP | HPI y/y | 5.50% | 5.20% | ||

| GBP | PPI Output m/m | -0.20% | -0.40% | ||

| 12:00 | EUR | German ZEW Economic Sentiment | 6.8 | 12.1 | |

| EUR | ZEW Economic Sentiment | 30.1 | 33.3 | ||

| 13:00 | USD | NFIB Small Business Index | 95.6 | 95.9 | |

| 21:00 | USD | Federal Budget Balance | 91.2B | -64.4B | |

| 14-Oct | 02:30 | AUD | Westpac Consumer Sentiment | -5.60% | |

| 02:50 | JPY | M2 Money Stock y/y | 4.30% | 4.20% | |

| JPY | PPI y/y | -3.90% | -3.60% | ||

| 04:30 | CNY | CPI y/y | 1.80% | 2.00% | |

| CNY | PPI y/y | -5.90% | -5.90% | ||

| 09:45 | EUR | French CPI m/m | -0.40% | 0.30% | |

| 11:30 | GBP | Average Earnings Index 3m/y | 3.10% | 2.90% | |

| GBP | Claimant Count Change | -2.3K | 1.2K | ||

| GBP | Unemployment Rate | 5.50% | 5.50% | ||

| 12:00 | CHF | ZEW Economic Expectations | 9.7 | ||

| EUR | Industrial Production m/m | -0.40% | 0.60% | ||

| 15:30 | USD | Core Retail Sales m/m | -0.10% | 0.10% | |

| USD | PPI m/m | -0.20% | 0.00% | ||

| USD | Retail Sales m/m | 0.20% | 0.20% | ||

| USD | Core PPI m/m | 0.10% | 0.30% | ||

| 17:00 | USD | Business Inventories m/m | 0.10% | 0.10% | |

| 21:00 | USD | Beige Book | |||

| 15-Oct | 00:30 | NZD | Business NZ Manufacturing Index | 55 | |

| 03:00 | AUD | MI Inflation Expectations | 3.20% | ||

| 03:30 | AUD | Employment Change | 7.2K | 17.4K | |

| AUD | Unemployment Rate | 6.20% | 6.20% | ||

| AUD | New Motor Vehicle Sales m/m | -1.60% | |||

| 07:30 | JPY | Revised Industrial Production m/m | -0.50% | -0.50% | |

| JPY | Tertiary Industry Activity m/m | 0.00% | 0.20% | ||

| Tentative | EUR | Spanish 10-y Bond Auction | 1.84|1.8 | ||

| 15:30 | USD | CPI m/m | -0.20% | -0.10% | |

| USD | Core CPI m/m | 0.10% | 0.10% | ||

| USD | Unemployment Claims | 269K | 263K | ||

| USD | Empire State Manufacturing Index | -7.3 | -14.7 | ||

| 17:00 | USD | Philly Fed Manufacturing Index | -1.8 | -6 | |

| 17:30 | USD | FOMC Member Dudley Speaks | |||

| USD | Natural Gas Storage | 95B | |||

| 18:00 | USD | Crude Oil Inventories | 3.1M | ||

| 16-Oct | 00:45 | NZD | CPI q/q | 0.20% | 0.40% |

| 03:30 | AUD | RBA Financial Stability Review | |||

| 11:00 | EUR | Italian Trade Balance | 4.23B | 8.03B | |

| 12:00 | EUR | Final CPI y/y | -0.10% | -0.10% | |

| EUR | Final Core CPI y/y | 0.90% | 0.90% | ||

| EUR | Trade Balance | 22.2B | 22.4B | ||

| 15:30 | CAD | Manufacturing Sales m/m | -0.60% | 1.70% | |

| CAD | Foreign Securities Purchases | 2.21B | -10.12B | ||

| 16:15 | USD | Capacity Utilization Rate | 77.40% | 77.60% | |

| USD | Industrial Production m/m | -0.20% | -0.40% | ||

| 17:00 | USD | Prelim UoM Consumer Sentiment | 88.8 | 87.2 | |

| USD | JOLTS Job Openings | 5.77M | 5.75M | ||

| USD | Prelim UoM Inflation Expectations | 2.80% | |||

| 23:00 | USD | TIC Long-Term Purchases | 7.7B |

Time: GMT+3

Currencies/Events to Watch this Week

Australia jobs report: After enjoying a stellar rally for the past few weeks the next major hurdle will be the monthly jobs report from Australia due on 15th October. Estimates call for the Australian unemployment rate to remain unchanged at 6.2% while the employment change is expected to rise 7.2k, a modest print from 17.4k print previously. For the most of the week, data from Australia is limited with NAB business confidence and Westpac consumer sentiment due earlier in the week.

Canadian Manufacturing sales: The monthly manufacturing sales data is due on the 16th of October, which incidentally happens to be the only main data point from Canada the week ahead. The median estimates expect a dip in manufacturing sales of -0.6%, down from a healthy 1.7% increase the month before. This week will also see a speech from the BoC Governor Poloz due to speak on late Monday. His comments will be of interest in light of the recent unemployment data from Canada which increased last week.

China inflation: The inflation data from China is due on 14th October with expectations of a slowdown from 2.0% last month to 1.8%. The producer price index is also due which is expected to post a decline of -5.9%. A weak CPI print is likely to keep the markets on the edge with China slowdown likely to take the forefront the coming week.

Eurozone Inflation: The various economies from the Eurozone will be releasing the inflation numbers this week. Germany’s final monthly CPI is expected to decline -0.2% while French CPI is expected to post steeper declines of -0.4%. The Eurozone annualized CPI data is also expected on 16th October with the median estimates pointing to a -0.1% decline on the headline and 0.9% on the core annualized CPI.

UK Jobs & Inflation: The UK’s inflation data is due on 13th October with expectations calling for a flat print. Unless the annualized headline CPI beats estimates the outlook seems to be bleak and one that could trigger speculation of a more dovish talk from the BoE in the coming months. On the core CPI however, estimates call for a 1.1% increase, up from 1.0% previously. On October 14th, the monthly jobs report from the UK is due. After a surprise improvement in the UK’s unemployment rate, expectations call for an unchanged print at 5.5% while the average earnings index is expected to rise 3.1%.

BoJ Monetary Policy: For the Japanese Yen, the week ahead looks quiet with no major economic releases. The Bank of Japan’s monetary policy meeting minutes are expected and markets will be looking to how the voting went in regards to keeping the QQE unchanged. Also this week, the producer price index and the revised industrial production numbers are due with expectations of -3.9% declines on the PPI and -0.5% decline in the industrial production data.

New Zealand Quarterly CPI: The Kiwi enjoyed a strong rebound last week and this rally will be put to the test as the quarterly CPI numbers are due on 16th October. Expectations call for a modest rise of 0.2%, lower than 0.4% CPI from a quarter ago. A beat on the estimates will likely put the Kiwi on the forefront. However, a miss on the CPI could see the NZDUSD take a strong hit as dovish sentiment on the NZDUSD creeps in with a view of further rate cuts from the RBNZ.

US Inflation and Retail sales: The US economy will be releasing details on the monthly retail sales numbers with dovish expectations of a decline of -0.1% on the core and an increase of 0.2% on the headline ahead of the monthly inflation numbers due on 15th October. The headline CPI for the month is expected to fall -0.2% while the core CPI is expected to remain steady at 0.1%. There are also a lot of FOMC member speeches due during the week which could bring additional volatility to the US Dollar.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)