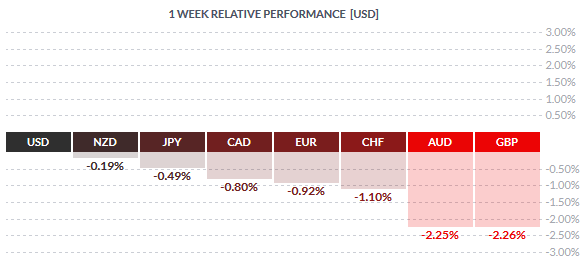

The US Dollar closed the week with the strongest gains across the board. The strength in the Greenback was largely on account of hawkish Fedspeak from various FOMC members who took the stage last week repeatedly reiterating the US Fed hike plans. The Kiwi dollar which was volatile last week came in as the second strongest currency with gains lifted by upward revised Fonterra payouts.

The Euro posted a second straight week of declines, losing a modest -0.29% for the week. However, it was the British Pound which was the weakest currency losing -2.26% to the Greenback followed by the Aussie dollar which lost -2.25%. The Aussie was largely dragged down by a sharp decline in various commodity prices.

Fundamentals for the Week 28/09 – 02/10

| Date | Time | Currency | Detail | Forecast | Previous |

| 28-09-15 | 15:30 | USD | FOMC Member Dudley Speaks | ||

| USD | Core PCE Price Index m/m | 0.10% | 0.10% | ||

| USD | Personal Spending m/m | 0.30% | 0.30% | ||

| USD | Personal Income m/m | 0.40% | 0.40% | ||

| 17:00 | USD | Pending Home Sales m/m | 0.40% | 0.50% | |

| 20:30 | USD | FOMC Member Evans Speaks | |||

| 29-09-15 | 00:00 | USD | FOMC Member Williams Speaks | ||

| 09:00 | EUR | German Import Prices m/m | -1.30% | -0.70% | |

| All Day | EUR | German Prelim CPI m/m | 0.00% | ||

| 10:00 | EUR | Spanish Flash CPI y/y | -0.60% | -0.40% | |

| 11:30 | GBP | Net Lending to Individuals m/m | 4.1B | 3.9B | |

| GBP | M4 Money Supply m/m | 0.70% | 1.00% | ||

| GBP | Mortgage Approvals | 70K | 69K | ||

| Tentative | EUR | Italian 10-y Bond Auction | 1.95|1.4 | ||

| 13:00 | GBP | CBI Realized Sales | 29 | 24 | |

| 15:30 | CAD | RMPI m/m | -5.90% | ||

| CAD | IPPI m/m | 0.70% | |||

| USD | Goods Trade Balance | -57.3B | -59.1B | ||

| 16:00 | USD | S&P/CS Composite-20 HPI y/y | 5.10% | 5.00% | |

| 17:00 | USD | CB Consumer Confidence | 96.2 | 101.5 | |

| 30-09-15 | 00:45 | NZD | Building Consents m/m | 20.40% | |

| 02:05 | GBP | GfK Consumer Confidence | 5 | 7 | |

| 02:50 | JPY | Retail Sales y/y | 1.30% | 1.80% | |

| JPY | Prelim Industrial Production m/m | 1.10% | -0.80% | ||

| 03:00 | NZD | ANZ Business Confidence | -29.1 | ||

| 04:30 | AUD | Building Approvals m/m | -1.90% | 4.20% | |

| AUD | Private Sector Credit m/m | 0.50% | 0.60% | ||

| 08:00 | JPY | Housing Starts y/y | 7.70% | 7.40% | |

| 09:00 | CHF | UBS Consumption Indicator | 1.64 | ||

| EUR | German Retail Sales m/m | 0.30% | 1.40% | ||

| GBP | Nationwide HPI m/m | 0.40% | 0.30% | ||

| 09:45 | EUR | French Consumer Spending m/m | 0.40% | ||

| Jul Data | EUR | French Consumer Spending m/m | 0.20% | 0.40% | |

| 10:00 | CHF | KOF Economic Barometer | 101.2 | 100.7 | |

| 10:55 | EUR | German Unemployment Change | -5K | -7K | |

| 11:00 | EUR | Italian Monthly Unemployment Rate | 12.00% | 12.00% | |

| 11:30 | GBP | Current Account | -22.3B | -26.5B | |

| GBP | Final GDP q/q | 0.70% | 0.70% | ||

| GBP | Index of Services 3m/3m | 0.80% | 0.70% | ||

| GBP | Revised Business Investment q/q | 2.90% | 2.90% | ||

| 12:00 | EUR | CPI Flash Estimate y/y | 0.00% | 0.10% | |

| EUR | Core CPI Flash Estimate y/y | 0.90% | 0.90% | ||

| EUR | Unemployment Rate | 10.90% | 10.90% | ||

| EUR | Italian Prelim CPI m/m | -0.20% | 0.20% | ||

| 15:00 | USD | FOMC Member Dudley Speaks | |||

| 15:15 | USD | ADP Non-Farm Employment Change | 191K | 190K | |

| 15:30 | CAD | GDP m/m | 0.20% | 0.50% | |

| 16:45 | USD | Chicago PMI | 53.2 | 54.4 | |

| 17:30 | USD | Crude Oil Inventories | -1.9M | ||

| 22:00 | USD | Fed Chair Yellen Speaks | |||

| 01-10-15 | 02:30 | AUD | AIG Manufacturing Index | 51.7 | |

| 02:50 | JPY | Tankan Manufacturing Index | 13 | 15 | |

| JPY | Tankan Non-Manufacturing Index | 21 | 23 | ||

| All Day | CNY | Bank Holiday | |||

| 03:00 | USD | FOMC Member Brainard Speaks | |||

| 04:00 | CNY | Manufacturing PMI | 49.7 | 49.7 | |

| CNY | Non-Manufacturing PMI | 53.4 | |||

| 04:35 | JPY | Final Manufacturing PMI | 50.9 | 50.9 | |

| 04:45 | CNY | Caixin Final Manufacturing PMI | 47.2 | 47 | |

| CNY | Caixin Services PMI | 51.2 | 51.5 | ||

| 06:45 | JPY | 10-y Bond Auction | 0.42|3.5 | ||

| 09:30 | AUD | Commodity Prices y/y | -20.90% | ||

| 10:15 | CHF | Retail Sales y/y | 0.30% | -0.10% | |

| EUR | Spanish Manufacturing PMI | 53 | 53.2 | ||

| 10:30 | CHF | Manufacturing PMI | 51.9 | 52.2 | |

| 10:45 | EUR | Italian Manufacturing PMI | 53.4 | 53.8 | |

| 10:50 | EUR | French Final Manufacturing PMI | 50.4 | 50.4 | |

| 10:55 | EUR | German Final Manufacturing PMI | 52.6 | 52.5 | |

| 11:00 | EUR | Final Manufacturing PMI | 52 | 52 | |

| 11:30 | GBP | Manufacturing PMI | 51.3 | 51.5 | |

| GBP | FPC Meeting Minutes | ||||

| Tentative | EUR | Spanish 10-y Bond Auction | 2.15|2.5 | ||

| Tentative | EUR | French 10-y Bond Auction | 1.21|1.7 | ||

| 14:30 | USD | Challenger Job Cuts y/y | 2.90% | ||

| 15:30 | USD | Unemployment Claims | 273K | 267K | |

| 16:30 | CAD | RBC Manufacturing PMI | 49.4 | ||

| 16:45 | USD | Final Manufacturing PMI | 53 | 53 | |

| 17:00 | USD | ISM Manufacturing PMI | 50.8 | 51.1 | |

| USD | Construction Spending m/m | 0.60% | 0.70% | ||

| USD | ISM Manufacturing Prices | 40 | 39 | ||

| 17:30 | USD | Natural Gas Storage | 106B | ||

| All Day | USD | Total Vehicle Sales | 17.5M | 17.8M | |

| 21:30 | USD | FOMC Member Williams Speaks | |||

| 02-10-15 | 02:30 | JPY | Household Spending y/y | 0.40% | -0.20% |

| JPY | Unemployment Rate | 3.30% | 3.30% | ||

| 02:50 | JPY | Monetary Base y/y | 34.20% | 33.30% | |

| All Day | CNY | Bank Holiday | |||

| 03:00 | NZD | ANZ Commodity Prices m/m | -5.20% | ||

| 04:30 | AUD | Retail Sales m/m | 0.40% | -0.10% | |

| 10:00 | EUR | Spanish Unemployment Change | 17.9K | 21.7K | |

| 11:30 | GBP | Construction PMI | 57.5 | 57.3 | |

| 12:00 | EUR | PPI m/m | -0.50% | -0.10% | |

| 15:30 | USD | Average Hourly Earnings m/m | 0.20% | 0.30% | |

| USD | Non-Farm Employment Change | 202K | 173K | ||

| USD | Unemployment Rate | 5.10% | 5.10% | ||

| 17:00 | USD | Factory Orders m/m | -0.90% | 0.40% |

Time: GMT+3

Currencies/Events to Watch this Week

Australia retail sales: Among other data during a relatively quiet week for the Aussie, the monthly retail sales data is forecasted to have grown at a pace of 0.4% for the month of September. The median estimates, point to a modest pickup in retail sales which declined -0.1% previously in August. Earlier in the week the monthly building approvals data is due, which is expected to show a decline of -1.9% after growing rapidly the month before at 4.2%. Although both these datasets do not account for much, the retail sales numbers could see some volatility in the Aussie currency pairs.

Canada GDP: The Canadian GDP is the only main event to look forward to for the week ahead. The median estimates forecast a slowdown to 0.2%, after the Canadian economy grew at a pace of 0.5% previously. Canada’s monthly GDP has been trending relatively flat with the exception of last month’s GDP. A better than or expected GDP print could be supportive to the Canadian dollar although the correlation to Crude oil prices has been stronger in recent weeks and has been the main driving factor.

China Manufacturing PMI: While data from China is quiet for the first part of the week, starting October 1st, focus will shift to the monthly PMI releases for both the manufacturing and non-manufacturing PMI numbers for the month of September. Expectations are for a near flat reading or unchanged from the previous month thus giving more scope for a possible beat on the estimates. In the unlikely event that the PMI’s continue to miss the median forecasts, it could potentially translate to another bout of uncertainty in the global equity markets as well as bring the Aussie and the Kiwi currencies under pressure.

German CPI and Eurozone flash CPI estimates: Data this week from Eurozone will see the monthly PMI data but the more important ones include the German CPI which is expected to stay unchanged. German retail sales are also due and is expected to post a soft print of 0.3%, down from 1.4% growth previously. Later in the week, the Eurozone flash CPI estimates are due for release with the median estimates pointing to a flat headline CPI of 0.0% while the core CPI is expected to be soft at 0.9% annualized.

UK Q2 Final GDP: The week ahead will see the final revised second quarter GDP results. Expectations are for an unchanged print of 0.7%. Last week, the US final revised GDP posted a strong upward revision of 3.9%, so a potential surprise with an upside revision to the UK’s GDP could help support the currency which has weakened considerably last week. Besides the GDP numbers, the monthly manufacturing and construction PMI data are also due for release.

US Nonfarm payrolls: The week ahead will be a busy one for the US with lot of economic releases on the agenda. However, the main event will be the monthly ADP private payroll numbers and the nonfarm payrolls due on Thursday and Friday. Expectations call for the unemployment rate to remain steady at 5.1% while the monthly job numbers is expected at 202k. Besides the unemployment data, many FOMC members continue the week with their speeches including Janet Yellen’s speech as well

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)