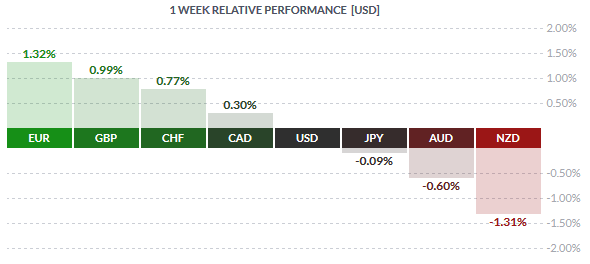

The Aussie and the Kiwi currencies were the worst performing last week led by the Yuan devaluation which dragged down with it most of the other Asian currencies as well. For the week, the Kiwi lost close to -1.31% followed by the Aussie dollar which was down -0.6%. Besides the Yuan devaluation, economic data from New Zealand continued to print weak numbers putting pressure on the Kiwi on all sides.

The Euro, single currency emerged on the top last week gaining 1.32% with the British Pound Sterling coming in at a close second with weekly gains of 0.99% The Euro was particularly stronger mostly due to the Greece debt negotiations coming through with a resolution to provide the country with its third bailout package ahead of August 20th repayment to the ECB. From the UK, a soft print on the monthly jobs report was the only major market event against a volatile Greenback which initially strengthened only to lose ground against the Euro and the British Pound.

Fundamentals for the Week August 14 – 21

| Date | Time | Currency | Detail | Forecast | Previous |

| 17-Aug | 02:01 | GBP | Rightmove HPI m/m | 0.10% | |

| 02:50 | JPY | Prelim GDP q/q | -0.50% | 1.00% | |

| JPY | Prelim GDP Price Index y/y | 2.20% | 3.40% | ||

| 10:15 | CHF | Retail Sales y/y | -0.60% | -1.80% | |

| 12:00 | EUR | Trade Balance | 19.3B | 21.2B | |

| 13:00 | EUR | German Buba Monthly Report | |||

| 15:30 | CAD | Foreign Securities Purchases | -5.45B | ||

| USD | Empire State Manufacturing Index | 5 | 3.9 | ||

| 17:00 | USD | NAHB Housing Market Index | 62 | 60 | |

| 23:00 | USD | TIC Long-Term Purchases | 93.0B | ||

| 04:30 | AUD | Monetary Policy Meeting Minutes | |||

| AUD | New Motor Vehicle Sales m/m | 3.80% | |||

| 18-Aug | 11:30 | GBP | CPI y/y | 0.00% | 0.00% |

| GBP | PPI Input m/m | -1.30% | -1.30% | ||

| GBP | RPI y/y | 0.90% | 1.00% | ||

| GBP | Core CPI y/y | 0.80% | 0.80% | ||

| GBP | HPI y/y | 5.90% | 5.70% | ||

| GBP | PPI Output m/m | -0.10% | 0.00% | ||

| 15:30 | USD | Building Permits | 1.21M | 1.34M | |

| USD | Housing Starts | 1.20M | 1.17M | ||

| Tentative | NZD | GDT Price Index | -9.30% | ||

| 01:45 | NZD | PPI Input q/q | -1.10% | ||

| NZD | PPI Output q/q | -0.90% | |||

| 19-Aug | 02:50 | JPY | Trade Balance | -0.16T | -0.25T |

| 03:30 | AUD | MI Leading Index m/m | 0.00% | ||

| 07:30 | JPY | All Industries Activity m/m | 0.40% | -0.50% | |

| 11:00 | EUR | Current Account | 19.2B | 18.0B | |

| 15:30 | USD | CPI m/m | 0.20% | 0.30% | |

| USD | Core CPI m/m | 0.20% | 0.20% | ||

| 17:30 | USD | Crude Oil Inventories | -1.7M | ||

| 21:00 | USD | FOMC Meeting Minutes | |||

| Tentative | JPY | Monetary Policy Statement | |||

| 09:00 | CHF | Trade Balance | 2.59B | 3.58B | |

| 20-Aug | EUR | German PPI m/m | 0.00% | -0.10% | |

| Tentative | JPY | BOJ Press Conference | |||

| 09:45 | USD | FOMC Member Williams Speaks | |||

| 11:30 | GBP | Retail Sales m/m | 0.20% | -0.20% | |

| 13:00 | GBP | CBI Industrial Order Expectations | -5 | -10 | |

| Tentative | EUR | Spanish 10-y Bond Auction | 1.98|1.7 | ||

| 15:30 | CAD | Wholesale Sales m/m | 0.20% | -1.00% | |

| USD | Unemployment Claims | 272K | 274K | ||

| 17:00 | USD | Philly Fed Manufacturing Index | 7.2 | 5.7 | |

| USD | Existing Home Sales | 5.45M | 5.49M | ||

| USD | CB Leading Index m/m | 0.20% | 0.60% | ||

| 17:30 | USD | Natural Gas Storage | 65B | ||

| 01:45 | NZD | Visitor Arrivals m/m | -0.20% | ||

| 04:35 | JPY | Flash Manufacturing PMI | 51.2 | ||

| 21-Aug | 04:45 | CNY | Caixin Flash Manufacturing PMI | 47.8 | |

| 06:00 | NZD | Credit Card Spending y/y | 6.50% | ||

| 09:00 | EUR | GfK German Consumer Climate | 10.2 | 10.1 | |

| 10:00 | EUR | French Flash Manufacturing PMI | 49.6 | ||

| EUR | French Flash Services PMI | 52 | |||

| 10:30 | EUR | German Flash Manufacturing PMI | 51.8 | ||

| EUR | German Flash Services PMI | 53.8 | |||

| 11:00 | EUR | Flash Manufacturing PMI | 52.4 | ||

| EUR | Flash Services PMI | 54 | |||

| 11:30 | GBP | Public Sector Net Borrowing | -2.3B | 8.6B | |

| 15:30 | CAD | Core CPI m/m | 0.00% | ||

| CAD | Core Retail Sales m/m | 0.90% | |||

| CAD | CPI m/m | 0.20% | |||

| CAD | Retail Sales m/m | 1.00% | |||

| 16:45 | USD | Flash Manufacturing PMI | 53.5 | 53.8 | |

| 17:00 | EUR | Consumer Confidence | -7 | -7 |

Currencies/Events to Watch this Week

RBA Meeting Minutes: The RBA will be releasing the meeting minutes on 18th August after it left interest rates unchanged at its last meeting earlier this month. The RBA’s rather neutral tone led to a strong surge in the Aussie and investors will look to any further clues from the RBA’s members on possibility of future interest rate changes.

New Zealand GDT prices and PPI: The Global Dairy trade price index is due on early Tuesday. Dairy prices have remained weak for the past few months and was one of the major reasons cited by the RBNZ for its rate cut. Therefore, the markets will look to see how the GDT prints numbers this time around after falling -9.3% previously. Also on the agenda is the quarterly producer price index which was weaker, posting -1.1% declines previously.

Japan Prelim GDP and BoJ Monetary policy: The preliminary GDP numbers from Japan are due this coming week with expectations biased to show the Japanese economy contracting by -0.5%. Also the BoJ will be meeting this week for its monetary policy which comes just a few days after the quarterly GDP release. The markets expect to see the BoJ maintain the status quo but a surprise weak print in the GDP could shift the balance.

Eurozone flash PMI’s: The week ahead could be a quiet week for the Euro with various Eurozone countries releasing the flash manufacturing and services PMI data. The Euro is likely to remain stronger in the coming week due to lack of any important market releases.

UK retail sales and CPI: The monthly consumer inflation data is due on Tuesday and expectations are dovish with the headline and core CPI expected to stay flat for the month. Retail sales numbers are also due this week with the median consensus pointing to a 0.2% growth after falling -0.2% last month.

Canada retail sales and CPI: The Canadian economic data has been largely mixed last week. The coming week will see the release of consumer inflation data which has remained flat at 0.0% on the core and 0.2% on the headline. Retail sales numbers are also due with the previous months showing a soft print of 1% and 0.9% on the headline and core respectively.

US FOMC minutes and CPI: The markets will get a glimpse into the Fed’s meeting minutes held in July and will be looking for further clues in regards to the impending rate hike plans. Monthly consumer inflation prices are also due for release with expectations on the soft side pointing to a 0.2% rise in inflation on both the headline and the core.