The markets this week will see the US and UK first estimates of the second quarter GDP for the year 2015. Heading into the release, the markets by and large remain vastly optimistic on the GDP’s for both the economies to have performed better than the previous quarter.

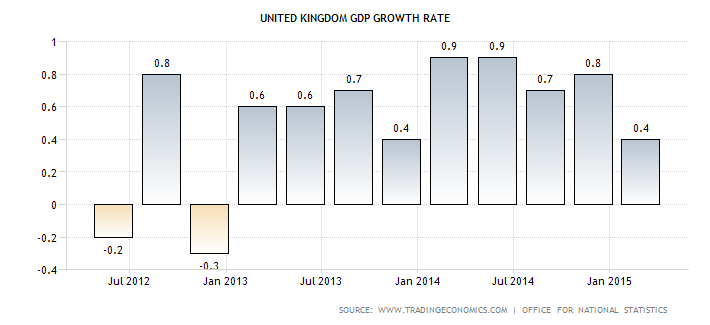

On July 28th, the UK’s GDP will be released first and expectations are that the UK’s economy grew at a pace of 0.7% during the second quarter, up from 0.4% previously (Q1 2015). On an annualized basis, the UK’s economy is expected to show a slightly softer growth of 2.6%, down from 2.9% previously. The previous revisions to the first quarter GDP were somewhat pessimistic, but by the third and final revision, the UK’s quarterly GDP was confirmed at 0.4%, albeit marking the slowest pace of growth since 2013.

The economic situation in the UK is currently understood to be well poised to take the risk of an interest rate hike from the Bank of England. Despite most of the BoE members staying unanimous in keeping interest rates steady at 0.5%, there has been a growing chorus of BoE members who have made hawkish speeches in recent events, thus increasing the likelihood of a rate hike from the UK in the medium term, with the markets pricing in a rate hike in early 2016, albeit expecting to see a rate hike by end of 2015.

The UK labor markets have been relatively strong over the past year, as the UK’s unemployment rate fell from the highs of 6.4% in early June 2014 to the current levels of 5.6% as of June 2015. At the same time, the average weekly earnings growth has also remained consistent, rising from below 0% growth in June 2014 to the current 3.2% weekly average earnings growth in June 2015.

However, the headline inflation has remained largely subdued which has been the main obstacle for raising rates. Inflation rate in the UK fell from 1.6% in July 2014, to a 0% flat growth rate since February this year. The core inflation rate, which ignores the volatile items such as Oil and gas, has been somewhat positive although staying weak. The UK’s core inflation rate fell from the highs of 1.9% in August 2014 to 0.8% in June 2015, clearly missing the BoE’s inflation rate target objective of maintaining a 2% inflation rate.

Considering the above, a pick up in the second quarter GDP would most likely encourage the BoE hawks in keeping the rhetoric alive for rate hikes in the near term. Although the GDP data is subject to revisions, it is now taken for granted that the next major policy change from the BoE will be a rate hike, thus ruling out any prospects of a rate cut, unless the UK economy starts to deteriorate in the remainder of this year.

The British Pound has been trading mostly stronger this year after its dramatic decline a year before. On a year to date basis, the Pound Sterling is currently down -0.3% against the Greenback and remains poised as one of the top currencies next to the US Dollar and the Swiss Franc that have been the strongest performing currencies this year.