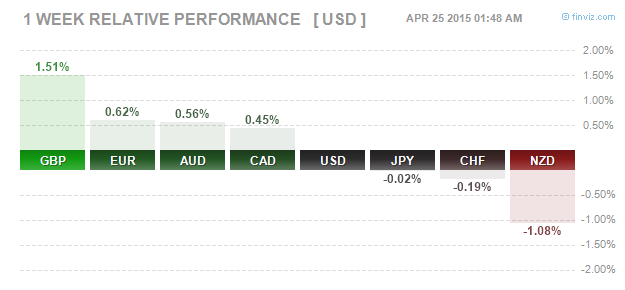

The British Pound was the comeback kid on the block as the currency soared this week, brushing aside election uncertainty risks. The British Pound’s rally however wasn’t based on any sound fundamentals. The BoE’s minutes did not show any major shifts in bias and a rate hike speculation hasn’t changed from the Q1 of 2016. Retail sales data was also weak, yet the Pound managed to beat its peers to race to the top of the board last week.

Figure 1: Weekly Spot FX Performance – 24/04/2015 (Source: Finviz.com)

The Kiwi Dollar and the Swiss Franc made it to the bottom of the currency charts last week due to central bank narratives. For the Kiwi, the RBNZ Assistant Governor came out strongly against the Kiwi’s rally which saw the currency plunge while the SNB Governor, Thomas Jordan widened the net for negative deposit rates to further weaken the Swiss Franc.

Fundamentals for the Week 27 April – 01 May

| Date | Time | Currency | Detail | Forecast | Previous | |

| 27-Apr | All Day | NZD | Bank Holiday | |||

| EUR | German Import Prices m/m | 1.40% | ||||

| 13:00 | GBP | CBI Industrial Order Expectations | 4 | 0 | ||

| 16:45 | USD | Flash Services PMI | 59.1 | 59.2 | ||

| 28-Apr | 01:40 | AUD | RBA Gov Stevens Speaks | |||

| 02:50 | JPY | Retail Sales y/y | -7.40% | -1.70% | ||

| 03:00 | AUD | CB Leading Index m/m | 0.40% | |||

| 11:30 | GBP | Prelim GDP q/q | 0.50% | 0.60% | ||

| GBP | BBA Mortgage Approvals | 37.9K | 37.3K | |||

| GBP | Index of Services 3m/3m | 0.70% | 0.80% | |||

| 15:45 | CAD | BOC Gov Poloz Speaks | ||||

| 16:00 | USD | S&P/CS Composite-20 HPI y/y | 4.70% | 4.60% | ||

| 17:00 | USD | CB Consumer Confidence | 102.6 | 101.3 | ||

| USD | Richmond Manufacturing Index | -2 | -8 | |||

| 29-Apr | 01:45 | NZD | Trade Balance | 312M | 50M | |

| All Day | JPY | Bank Holiday | ||||

| 04:00 | NZD | ANZ Business Confidence | 35.8 | |||

| 09:00 | CHF | UBS Consumption Indicator | 1.19 | |||

| GBP | Nationwide HPI m/m | 0.10% | ||||

| All Day | EUR | German Prelim CPI m/m | -0.10% | 0.50% | ||

| 11:00 | EUR | M3 Money Supply y/y | 4.30% | 4.00% | ||

| EUR | Private Loans y/y | 0.20% | -0.10% | |||

| Tentative | EUR | Italian 10-y Bond Auction | 1.34|1.5 | |||

| Tentative | GBP | 10-y Bond Auction | 1.68|1.4 | |||

| 13:00 | GBP | CBI Realized Sales | 26 | 18 | ||

| 15:30 | CAD | RMPI m/m | -1.80% | 6.10% | ||

| CAD | IPPI m/m | -0.10% | 1.80% | |||

| USD | Advance GDP q/q | 1.00% | 2.20% | |||

| USD | Advance GDP Price Index q/q | 0.50% | 0.10% | |||

| 17:00 | USD | Pending Home Sales m/m | 1.10% | 3.10% | ||

| 17:30 | USD | Crude Oil Inventories | 5.3M | |||

| 21:00 | USD | FOMC Statement | ||||

| USD | Federal Funds Rate | <0.25% | <0.25% | |||

| 30-Apr | 00:00 | NZD | Official Cash Rate | 3.50% | 3.50% | |

| NZD | RBNZ Rate Statement | |||||

| 01:45 | NZD | Building Consents m/m | -6.30% | |||

| 02:05 | GBP | GfK Consumer Confidence | 5 | 4 | ||

| 02:50 | JPY | Prelim Industrial Production m/m | -3.40% | -3.10% | ||

| 04:30 | AUD | Import Prices q/q | 1.10% | 0.90% | ||

| AUD | Private Sector Credit m/m | 0.50% | 0.50% | |||

| Tentative | JPY | Monetary Policy Statement | ||||

| 08:00 | JPY | Housing Starts y/y | -1.80% | -3.10% | ||

| 09:00 | EUR | German Retail Sales m/m | 0.50% | -0.10% | ||

| JPY | BOJ Outlook Report | |||||

| Tentative | JPY | BOJ Press Conference | ||||

| 09:45 | EUR | French Consumer Spending m/m | -0.50% | 0.10% | ||

| 10:00 | CHF | KOF Economic Barometer | 91.7 | 90.8 | ||

| EUR | Spanish Flash CPI y/y | -0.70% | -0.70% | |||

| EUR | Spanish Flash GDP q/q | 0.80% | 0.70% | |||

| 10:55 | EUR | German Unemployment Change | -14K | -15K | ||

| 11:00 | EUR | ECB Economic Bulletin | ||||

| EUR | Italian Monthly Unemployment Rate | 12.60% | 12.70% | |||

| 12:00 | EUR | CPI Flash Estimate y/y | 0.00% | -0.10% | ||

| EUR | Core CPI Flash Estimate y/y | 0.60% | 0.60% | |||

| EUR | Unemployment Rate | 11.20% | 11.30% | |||

| EUR | Italian Prelim CPI m/m | 0.20% | 0.10% | |||

| 15:30 | CAD | GDP m/m | -0.20% | -0.10% | ||

| USD | Unemployment Claims | 297K | 294K | |||

| USD | Core PCE Price Index m/m | 0.20% | 0.10% | |||

| USD | Employment Cost Index q/q | 0.60% | 0.60% | |||

| USD | Personal Spending m/m | 0.60% | 0.10% | |||

| USD | Personal Income m/m | 0.20% | 0.40% | |||

| 16:45 | USD | Chicago PMI | 50.1 | 46.3 | ||

| 17:30 | CAD | BOC Gov Poloz Speaks | ||||

| USD | Natural Gas Storage | 90B | ||||

| 01-May | 02:30 | AUD | AIG Manufacturing Index | 46.3 | ||

| JPY | Household Spending y/y | -11.70% | -2.90% | |||

| JPY | Tokyo Core CPI y/y | 0.50% | 2.20% | |||

| JPY | National Core CPI y/y | 2.00% | 2.00% | |||

| JPY | Unemployment Rate | 3.50% | 3.50% | |||

| All Day | CNY | Bank Holiday | ||||

| 04:00 | CNY | Manufacturing PMI | 50 | 50.1 | ||

| CNY | Non-Manufacturing PMI | 53.7 | ||||

| 04:30 | AUD | PPI q/q | 0.20% | 0.10% | ||

| JPY | Average Cash Earnings y/y | 0.40% | 0.10% | |||

| 04:35 | JPY | Final Manufacturing PMI | 49.8 | 49.7 | ||

| All Day | CHF | Bank Holiday | ||||

| All Day | EUR | French Bank Holiday | ||||

| All Day | EUR | German Bank Holiday | ||||

| All Day | EUR | Italian Bank Holiday | ||||

| 09:30 | AUD | Commodity Prices y/y | -19.70% | |||

| 11:30 | GBP | Manufacturing PMI | 54.6 | 54.4 | ||

| GBP | Net Lending to Individuals m/m | 2.6B | 2.5B | |||

| GBP | M4 Money Supply m/m | 0.10% | -0.20% | |||

| GBP | Mortgage Approvals | 63K | 62K | |||

| 16:45 | USD | Final Manufacturing PMI | 54.2 | 54.2 | ||

| 17:00 | USD | ISM Manufacturing PMI | 52.1 | 51.5 | ||

| USD | Revised UoM Consumer Sentiment | 96.1 | 95.9 | |||

| USD | Construction Spending m/m | 0.50% | -0.10% | |||

| USD | ISM Manufacturing Prices | 42.3 | 39 | |||

| USD | Revised UoM Inflation Expectations | 2.50% | ||||

| All Day | USD | Total Vehicle Sales | 16.9M | 17.2M | ||

Currencies/Events to Watch this Week

UK Q1 2015 GDP estimates: Will the British Pound manage to keep up its rally the coming week? The most important data on the table the coming week is the first quarter GDP estimates. Consensus is for a 0.5% growth a soft print from 0.6% in Q4 of 2014. Also this week marks the final week ahead of the UK elections due the week later on May 7th. Expect to see some volatility across the GBP crosses in the coming weeks.

BoJ – Monetary easing on the cards? The Bank of Japan meets on April 30th and there is a finely divided consensus that the Bank of Japan could spring a surprise by expanding its monetary policy stimulus from the current 80trillion Yen to 90trillion Yen. While on the other hand, consensus calls for an expansion few months later in either June or July. The markets will be looking to the BoJ in this aspect and any surprises could see the Yen weaken considerably.

Will RBNZ strike a dovish bias? After last week’s comments from John McDermott, the assistant governor, the RBNZ’s monetary policy decision will be an important one to watch. The big question is how the RBNZ will tone its statement. While there are no expectations for any interest rate change, the markets will be focusing on the forward guidance from the New Zealand Central bank.

US advance GDP, FOMC meeting: April 30th will likely turn out to be a volatile day as far as the Greenback is concerned. The major high risk events include the advance GDP which is estimated to be at a soft 1% and is followed by later by the FOMC meeting. There is no press conference during this meeting and it will be interesting to see how the FOMC will tone its monetary policy statement. Will the Fed remain optimistic about the economy or will it voice concerns about the slowdown in the first quarter of 2015?

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)