Weekly Forex Forecast for 20-24 April 2015 features the following:

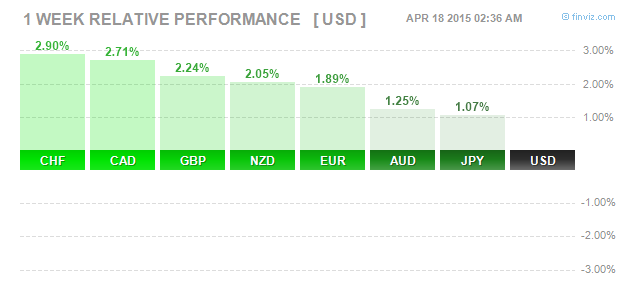

The US Dollar was noticeably the weakest currency the last week with the Swiss Franc and the Canadian Dollar taking the top spots. The British Pound made a comeback this week as the currency managed to erase some of its losses from the past few weeks. However election uncertainty continues to weigh down the currency and volatility in the British Pound may pick up as the UK election date gets closer.

Figure 1: Weekly Spot FX Performance – 17/04/2015 (Source: Finviz.com)

The US Dollar saw sharp reactionary sell offs as and when economic data disappointed. The most evident was retail sales, which failed to meet estimates but saw a rebound from the previous months, and Core CPI y/y continued to be stronger at 1.8%, yet the Dollar did not budge on the news. The coming weeks could prove to be an interesting time for the Greenback especially as seasonal tendencies are in the favor of a weaker Greenback for the coming months.

Fundamentals for the Week 20 – 24 April

| Date | Time | Currency | Detail | Forecast | Previous |

| 20-Apr | 01:45 | NZD | CPI q/q | -0.20% | -0.20% |

| 02:01 | GBP | Rightmove HPI m/m | 1.00% | ||

| 02:50 | JPY | Tertiary Industry Activity m/m | -0.60% | 1.40% | |

| 09:00 | EUR | German PPI m/m | 0.20% | 0.10% | |

| 13:00 | EUR | German Buba Monthly Report | |||

| 17:05 | CAD | BOC Gov Poloz Speaks | |||

| 19:30 | AUD | RBA Gov Stevens Speaks | |||

| 21-Apr | 04:30 | AUD | Monetary Policy Meeting Minutes | ||

| 12:00 | EUR | German ZEW Economic Sentiment | 56 | 54.8 | |

| EUR | ZEW Economic Sentiment | 63.7 | 62.4 | ||

| Tentative | GBP | 30-y Bond Auction | 2.36|1.6 | ||

| 15:30 | CAD | Wholesale Sales m/m | -3.10% | ||

| 23:00 | CAD | Annual Budget Release | |||

| 22-Apr | 02:50 | JPY | Trade Balance | -0.41T | -0.64T |

| 03:30 | AUD | MI Leading Index m/m | 0.30% | ||

| 04:30 | AUD | CPI q/q | 0.10% | 0.20% | |

| AUD | Trimmed Mean CPI q/q | 0.60% | 0.70% | ||

| 05:00 | CNY | CB Leading Index m/m | 1.50% | ||

| 11:30 | GBP | MPC Official Bank Rate Votes | 0-0-9 | 0-0-9 | |

| GBP | MPC Asset Purchase Facility Votes | 0-0-9 | 0-0-9 | ||

| 12:00 | CHF | ZEW Economic Expectations | -37.9 | ||

| EUR | Italian Retail Sales m/m | 0.30% | 0.10% | ||

| 16:00 | USD | HPI m/m | 0.70% | 0.30% | |

| 17:00 | EUR | Consumer Confidence | -3 | -4 | |

| USD | Existing Home Sales | 5.04M | 4.88M | ||

| 17:30 | USD | Crude Oil Inventories | 1.3M | ||

| 23-Apr | 01:45 | NZD | Visitor Arrivals m/m | 6.90% | |

| 04:30 | AUD | NAB Quarterly Business Confidence | 2 | ||

| 04:35 | JPY | Flash Manufacturing PMI | 50.8 | 50.3 | |

| 04:45 | CNY | HSBC Flash Manufacturing PMI | 49.4 | 49.6 | |

| 06:00 | NZD | Credit Card Spending y/y | 5.80% | ||

| 09:00 | CHF | Trade Balance | 2.16B | 2.47B | |

| 10:00 | EUR | French Flash Manufacturing PMI | 49.4 | 48.8 | |

| EUR | French Flash Services PMI | 52.5 | 52.4 | ||

| EUR | Spanish Unemployment Rate | 23.50% | 23.70% | ||

| 10:30 | EUR | German Flash Manufacturing PMI | 53.1 | 52.8 | |

| EUR | German Flash Services PMI | 55.6 | 55.4 | ||

| 11:00 | EUR | Flash Manufacturing PMI | 52.6 | 52.2 | |

| EUR | Flash Services PMI | 54.5 | 54.2 | ||

| 11:30 | GBP | Retail Sales m/m | 0.40% | 0.70% | |

| GBP | Public Sector Net Borrowing | 6.6B | 6.2B | ||

| 15:30 | USD | Unemployment Claims | 290K | 294K | |

| 16:45 | USD | Flash Manufacturing PMI | 55.6 | 55.7 | |

| 17:00 | USD | New Home Sales | 514K | 539K | |

| 17:30 | USD | Natural Gas Storage | 63B | ||

| 24-Apr | 02:50 | JPY | SPPI y/y | 3.30% | 3.30% |

| 07:30 | JPY | All Industries Activity m/m | -0.90% | 1.90% | |

| 11:00 | EUR | German Ifo Business Climate | 108.5 | 107.9 | |

| All Day | EUR | Eurogroup Meetings | |||

| 15:30 | USD | Core Durable Goods Orders m/m | 0.20% | -0.60% | |

| USD | Durable Goods Orders m/m | 0.70% | -1.10% | ||

| 16:00 | EUR | Belgian NBB Business Climate | -5.8 | -6.3 | |

| 17:30 | CAD | BOC Gov Poloz Speaks |

Currencies/Events to Watch this Week

Australia quarterly inflation: The RBA did not cut rates and the recent jobs report was stronger. The final piece to the puzzle is this week’s quarterly CPI data which has been in a downtrend slowing down to 0.5%. A rebound or at the very least, no change to the quarterly CPI is all that is needed to seal the deal for the RBA to leave policy unchanged in May. Ahead of CPI data, the Aussie is likely to be susceptible to the RBA meeting minutes for April and there’s a speech from RBA Governor, Glenn Stevens ahead of both the events.

Eurogroup Meeting – April 24th: The Eurogroup members will meet in Riga, Latvia on April 24th and Greece tops the agenda. There have been rumors floating that the Eurozone was preparing a Grexit plan which was backtracked and these rumors continue to add to the speculation. The end of the month, Greece is expected to make another big payment and the cash-strapped country has been leaving no stone unturned to gain funding. Germany watered down any expectations from the April 24th meeting that nothing significant could come out of that meeting. The Euro is likely to keep track of the events this week and could be quite volatile.

Calm week for the Greenback: After a data heavy last week, the Greenback see’s a period of quiet with no major market moving events scheduled. The only exception being the Core durable goods orders due on Friday. Expectations are for a modest rebound after orders fell -0.6% previously. A worse than expected print could potentially see further declines in the Greenback and could possibly seal the deal for the Greenback looking for a stronger support at lower levels before it can hope to break the 100 psychological and round number resistance level.