The currency markets saw a volatile first quarter of the year with Central Bank monetary policies taking center stage. Expectations shifted back and forth in regards to economies as speculation for interest rate hikes and cuts continued to be the main driving force.

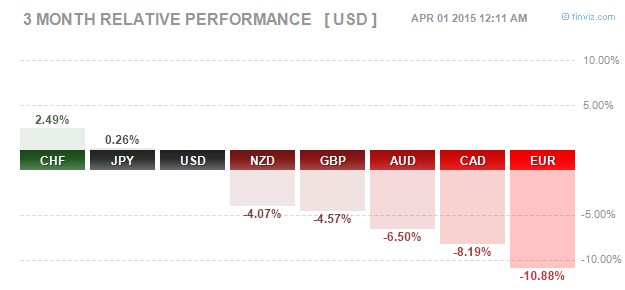

Figure 1: Forex - Quarterly Performance, Jan – Mar, 2015

Here is a forex quarterly review of the main market events from the first months of 2015.

Swiss National Bank abandons the 1.20Euro Peg

The Swiss National Bank was the first mover amongst Central banks as the SNB President; Thomas Jordan announced that the SNB would no longer defend the EURCHF peg at 1.20. A move that surprised and shocked the markets, leading to a mini flash crash in the currency markets, the Swiss Franc, often seen as a safe haven bet, rallied close to 18% on the day, against the Euro. The move by the SNB was a precursor to the fact that the ECB was going to ready its QE Bazooka few weeks later.

Ever since, the Swiss Franc managed to stabilize with the pair briefly flirting with the highs of 1.08 after reaching lows of 0.97.

ECB’s QE Bazooka

The European Central bank got a shot in the arm when few weeks before its crucial January monetary policy meeting, the European Court of Justice gave its ruling that the sovereign bond purchases was legal and within the EU’s mandate. This put to rest any remaining doubts on the ECB’s QE plans where Germany was hitherto a staunch opponent to the idea. The ECB announced that it would embark on an open ended bond purchase program, amounting to 60 billion Euros worth of bond purchases every month starting March through September 2016. The ECB also noted that it would continue the QE program beyond September if the economy warrants further monetary support.

Given the speculation of the ECB’s QE program, the Euro was weakening even months before the announcement but saw a dramatic decline. The Euro lost close to -11% against the Greenback, dropping from the psychological round number of 1.20.

US Federal Reserve is now reasonably confident of a rate hike

The US Federal Reserve removed the word “patience” from its statement replacing it with “reasonably confident” putting the rate hike live, any time from its June monetary policy meeting. Buoyed by a pickup in unemployment rate and confident that inflation would rise back towards the Fed’s target rate of 2%, the FOMC confirmed to the markets in March that it would be looking to normalize interest rates soon.

The US Dollar Index which has been in a strong parabolic incline continued to rise further, gaining close to 8% for the quarter after briefly flirting with the psychological resistance level of 100.

Markets are however a bit confused as certain economic indicators in the US economy have failed to meet up with the expectations and the fact that the rising US Dollar has been hurting exports was also mentioned by the Fed.

No matter what, the FOMC will be a much watched event come May.

RBA cuts rates – Dovish outlook

The Reserve Bank of Australia cut interest rates in February by 25bps, taking the benchmark rates from 2.5% to 2.25%, citing lower growth and signs of inflation weakening. The main threat to the RBA’s rate cuts come from the property markets which have already started showing signs of heating up. Further rate cuts are most likely going to be difficult to maneuver between stimulating growth and encourage borrowing while at the same time keeping an eye on the housing markets least it ends up in a bubble.

The RBA also continued to stick to its rhetoric of talking down the Australian dollar citing lower commodity prices.

The Australian dollar has weakened close to -7% since the start of the quarter as the markets turn bearish on the AUD with expectations of another 25bps rate cut in the next quarter.

Bank of Canada cuts rates as a precaution

The Bank of Canada’s rate cut turned out to be a major surprise in the markets in February. The Boc slashed interest rates by 25bps from 1% to 0.75%. Subsequent comments from BoC Governor Poloz however showed that the rate cut decision was taken as a means of insurance against the decline in Crude oil prices and the subdued growth in Canada.

The Canadian Dollar, which is influenced by the Crude oil prices has lost as much as -9.5% against the Greenback, trading near 1.28 levels. The surprise rate cut has led to further speculation of another follow up rate cut in Q2.

Bank of England – Steady as she goes

The Bank of England was perhaps the sole steady ship from the lot (besides the BoJ) in this quarter with no major monetary policy decisions being made. This was something which we noted previously few months ago as Central Banks are usually hesitant to take any major decisions before a general election. In this aspect, the BoE could continue to maintain the status quo until the May elections are done with.

However, BoE officials were quite verbal in the past few months, sometimes talking about the risks of an appreciating Pound and talking about the possibility of a rate cut and at times coming out hawkish on the monetary policies.

The UK will hold its general elections in May and the British Pound is either going to move sideways for the most part or weaken in the run up to the elections as opinion polls strongly suggests another collation government being formed as the most likely outcome.

The British Pound has lost close to -5% against the Greenback for the quarter.

Bank of Japan – An uneventful Q1

The Bank of Japan surprisingly refused to budge on its monetary policy decisions and instead painted an optimistic outlook on inflation despite the global headwinds coming from falling oil prices that has lowered inflation expectations across most of the countries.

The BoJ especially left its policy unchanged in March ahead of the key spring wage negotiations which showed most of the companies offering better wages, making it a second consecutive year of wage growth, something which both the BoJ Governor Kuroda and Japanese Premier Shinzo Abe have been campaigning for.

The big question however is will the wage growth be enough to help boost inflation which has been a drag on the Japanese economy.

The second quarter of the year could probably see some whispers of a possible expansion to the BoJ’s QE policy. The Yen was one of the best performing currencies across the board with the exception of the Greenback. For the quarter USDJPY barely made any significant gains or profits, closing in near the 120 levels.