Weekly Forex Forecast: 9th to 13th February

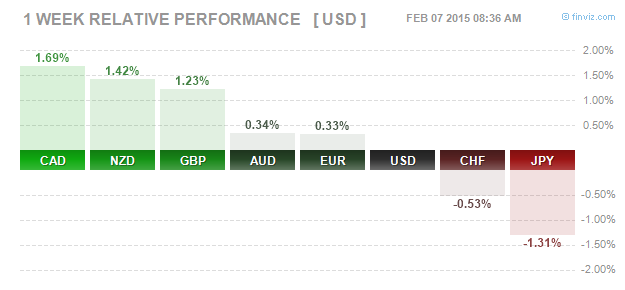

A major rebound in Crude oil prices managed to help lift off the currency markets with the Canadian dollar leading the way, gaining as much as 1.6% against the Greenback while also supporting the Kiwi Dollar. The surprise shift in sentiment came from the British Sterling, which rose 1.23% for the week against the Greenback ahead of the NFP release.

US Jobs data beat estimates and was seen as largely bullish by the markets. Although the unemployment rate rose to 5.7%, it was offset by over 147k+ revisions to the past NFP numbers bringing back to front the USD bulls. The Dollar Index managed to trim its losses for the week practically ending near the weekly open.

The Euro, the single currency which managed to top the week before was weaker last week as it managed to rise only 0.33% as the currency gave away its gains on an upbeat NFP data.

Fundamentals for the Week 9 – 13 Feb

| Date | Event | Estimates |

| 9 February | RBA Gov. Stevens Speech | – |

| Japan consumer confidence | 39.4 | |

| Japan economy watchers sentiment | 45.7 | |

| Eurozone Sentix investor confidence | 3.4 | |

| Canada housing starts | 184k | |

| US Labor Markets condition index m/m | 6.1 | |

| 10 February | Australia NAB business confidence | 2 |

| Australia HPI q/q | 2% | |

| China CPI y/y | 1.1% | |

| China PPI y/y | -3.7% | |

| Switzerland unemployment rate | 3.2% | |

| French industrial production m/m | 0.3% | |

| UK Manufacturing production m/m | 0.3% | |

| UK Industrial production m/m | 0.3% | |

| NFIB small business index (US) | 101.3 | |

| NIESR GDP estimate (UK) | 0.6% | |

| JOLTS Job openings | 5.03mn | |

| US Wholesale inventories m/m | 0.2% | |

| IBD/TIPP economic optimism | 51.4 | |

| 11 February | Japan Bank holiday | – |

| Australia home loans m/m | 2.3% | |

| US Federal Budget balance | -2.6bn | |

| New Zealand manufacturing index | 57.7 | |

| 12 February | RBA Asst. Governor Speech | – |

| Japan core machinery orders m/m | 2.4% | |

| Japan PPI y/y | 1.2% | |

| Australia inflation expectations | – | |

| Australia unemployment change | -4.7k | |

| Australia unemployment rate | 6.2% | |

| German final CPI m/m-1% | 56.6 | |

| Eurozone industrial production m/m | 0.3% | |

| BoE Carney speech | – | |

| BoE inflation report | – | |

| Canada NHPI m/m | 0.2% | |

| US Core retail sales m/m | -0.4% | |

| US Retail sales m/m | -0.3% | |

| Business inventories | 0.2% | |

| 13 February | RBA Gov. Stevens speech | – |

| French prelim GDP q/q | 0.1% | |

| German prelim GDP q/q | 0.3% | |

| Italy prelim GDP q/q | 0% | |

| Eurozone Flash GDP q/q | 0.2% | |

| Canada manufacturing sales m/m | -0.9% | |

| US Import prices m/m | -3.1% | |

| UoM consumer sentiment | 98.2 | |

| UoM inflation expectations | – |

Currencies/Events to Watch this Week

China Inflation numbers: With the PBOC cutting its reserve requirements ratio last week, the markets are speculating that China will be the next in line to cut interest rates, a view that is likely to find ground this week as China reports its yearly inflation numbers on Tuesday the 10th. Expectations are down with a 1.1% rise in inflation against previous 1.5%. A miss of the estimates could strengthen the view of a potential rate cut from China.

Euro: There are no major events scheduled for the Eurozone for most of this week with the exception of Friday which will see the preliminary quarterly GDP numbers from Italy, France and Germany as well as the Eurozone composite GDP numbers. Expectations are tilted to the downside, so any surprise prints in the positive could help support the Euro.

British Pound: The BoE will be holding its quarterly inflation report hearing and the markets will also get to learn more about the inflation letter from BoE Governor Mark Carney to the UK Chancellor, explaining the reasons why inflation missed the Central Bank’s targets. Of importance will be the BoE’s view on inflation expectations. Manufacturing and industrial production data are also due from the UK.

Australian Dollar: The week starts off with a speech by RBA Governor Stevens, which could likely see potential “talking down” of the Aussie, which poses a main risk. Business confidence data is due from Australia alongside the monthly labor market data, which is expected to bring some volatility to the Australian Dollar. China’s inflation data may also particularly impact the Aussie and the Kiwi Dollars.

FX Majors Weekly Pivots

| R3 | R2 | R1 | Pivot | S1 | S2 | S3 | |

| EURUSD | 1.1713 | 1.1623 | 1.1472 | 1.1381 | 1.1230 | 1.1140 | 1.0988 |

| GBPUSD | 1.5763 | 1.5558 | 1.54 | 1.5194 | 1.5036 | 1.4830 | 1.4672 |

| USDCAD | 1.3168 | 1.2970 | 1.2747 | 1.2549 | 1.2325 | 1.2128 | 1.1904 |

| USDJPY | 122.164 | 120.692 | 119.820 | 118.348 | 117.476 | 116.004 | 115.132 |

| AUDUSD | 0.8161 | 0.8019 | 0.7911 | 0.7768 | 0.7660 | 0.7518 | 0.7410 |

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)