As the currency markets progress into the final weeks of July, the main highlights of the week include the FOMC meeting on Wednesday. The Fed is expected to keep monetary policy on hold. Investors are likely to focus on any forward guidance that will be issued by the Fed this week. Questions still remain on the pace of rate hikes as well the balance sheet normalization.

Elsewhere, traders will turn their attention to the quarterly inflation report from Australia. Following the disappointing inflation figures from New Zealand last week, the Australia CPI will be an important data point.

The UK will be seeing the preliminary GDP report this week as well. The data covers the second quarter ending June. Considering that the first GDP estimate will often be revised, the data could, however, pressure the British pound on expectations of a weaker pace of GDP growth.

FOMC Monetary Policy Meeting – No changes expected

The Federal Reserve will be holding its monthly monetary policy meeting this week. The meeting will only include the statement from the central bank with no press conference. As a result, the FOMC meeting this week is expected to be a low key affair.

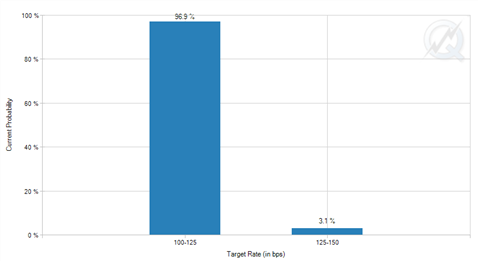

No changes are expected as far as the short term interest rates are concerned. The Fed funds rates currently stand at 1% – 1.25%. According to the CME Group’s Fed funds rate probability, the expectations from the July 26 meeting assigns just a 3% probability of a rate hike, with over 97% expecting the Fed funds rate to stay unchanged.

Traders will be particularly focused on the FOMC statement. The forward guidance will be key as to what the Fed will do over the coming months. So far, Fed officials have remained quiet as far as the future of interest rate hikes is concerned. The Fed projects one more rate hike this year, but traders are skeptical about this.

The FOMC statement is also likely to focus on the Fed’s balance sheet normalization. Further details could be given on this which could balance the dovishness from keeping interest rates steady. Various officials are in favor of starting with unwinding the balance sheet while interest rates remain at the current levels.

Australia inflation expected to remain muted

Australia will be releasing the second quarter inflation data this week. Expectations from the economists’ poll, put the inflation rate in the second quarter to remain subdued with inflationary pressures being muted.

This is expected to bring the yearly inflation rate to around 2.3% and 0.5% on a quarterly basis. Despite the muted inflation, Australia’s consumer prices remain well anchored within the central bank’s 2% – 3% target rate.

Last week, the RBA Deputy Governor Debelle gave a speech. He said that there was nothing new to conclude as far as policy decisions were concerned. His comments sent the Australian dollar lower on the day.

RBA’s deputy governor told an audience, speaking in Adelaide, not to give too much significance to the discussions from the RBA’s minutes. He further went to say that the minutes were merely procedural. Debelle said that there was nothing compelling the RBA to follow the tightening path that other central banks were preparing for and reminded the audience that the RBA’s policy was more focused on the domestic fundamentals.

UK quarterly GDP expected to rise

The preliminary GDP data for the UK for the period of the three months ending June or Q2 will be released by the UK’s Office for National Statistics (ONS) this week. According to economists polled, expectations call for a modest increase of 0.3% on a quarterly basis in the economy.

On a year over year basis, however, the UK’s annual GDP rate is expected to rise at a pace of 1.7%. This is slower than the 2% increase that was registered in the first quarter. The slight pickup in the GDP is expected based on the resilient economy. Despite facing headwinds such as wage pressures and rising inflation, the UK economy is expected to weather the short-term effect.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)