The week ahead will open in the backdrop of the French elections which will be the main overriding theme. Monday is a bank holiday in Australia and New Zealand.

Traders will be focusing on the ECB and the BoJ’s meetings this week. No changes are expected from both these meetings this week with the respective central bank chiefs likely to reiterate that monetary policy will remain accommodative and appropriate to the current conditions.

The U.S. advance GDP report will be coming out this week for the first quarter of 2017, while Australia will be reporting on the quarterly inflation numbers. Here’s a brief preview of this week’s economic events.

U.S. first quarter GDP expected to slow

Economic data from the United States next week will focus on the first quarter gross domestic product (GDP). Economists are expecting to see the first quarter GDP rise 1.2% at an annual rate. This expected to be significantly lower than the 2.1% increase registered in the fourth quarter of 2016.

The first quarter GDP growth in the U.S. is typically weak on a seasonal basis, and thus, the trend is expected to continue. However, for the market participants, this could be a bit of recalibration on the expectations from the Federal Reserve.

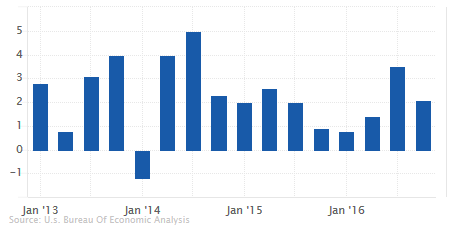

Besides the GDP data, the focus will also be on the employment cost index (ECI) for the first quarter. This is likely to be a more important factor for the markets as the Fed will be looking at the amount of slack in the labor market during the three months ending March.

Private industry wages increased 2.5% on year over year basis in the fourth quarter of 2016

The U.S. durable goods orders will also be released this week with estimates showing a 0.5% increase on the core durable goods orders and a 1.5% increase on the headline print.

European central bank expected to stay on the sidelines

With the French elections results from the first round in the background, the European central bank’s monetary policy meeting this week is expected to remain a non-event as interest rates and QE is expected to remain unchanged at this week’s meeting.

Given the slow pace of increase in inflation, the ECB is likely to maintain an accommodative policy noting that the downside risks still exists, especially after the core inflation rate rose 0.7%, slower than 0.8% that was registered in the previous months.

Furthermore, most of the gains in the inflation seem to be on account of a slide in energy prices, which is likely to see the ECB officials maintain an accommodative monetary policy until the inflation objective is met.

Besides the ECB meeting, France and Spain will be releasing the preliminary GDP numbers for the first quarter. Economists are expecting the French GDP to post a modest decline while Spain GDP is expected to improve from the previous quarter

No changes expected from the Bank of Japan

The Bank of Japan’s monetary policy meeting this week is expected to see no major surprises including maintaining the bond purchases at the pace of 80 trillion yen annually and the interest rate at -0.10%.

BoJ Governor Kuroda in a recent speech reiterated the BoJ’s stance of maintaining its aggressive easing policy.

Despite some initial rhetoric of tightening from the BoJ, the weak pace of inflation is expected to keep BoJ officials on the sidelines with inflation still remaining zero-bound. The markets will also be speculating on the term for BoJ’s Kuroda whose position as the central bank governor could be extended by Shinzo Abe for another five years.

The BoJ has also maintained a steady pace of purchases on the 10-year Japanese Government Bonds (JGB’s) which also rules out any speculative of premature tapering from the BoJ.