- Japan all industry activity falls on weaker construction and industrial output

- RBNZ releases economic report suggesting further easing was required

- Australia NAB business confidence falls in Q2

- UK retail sales falls to a 6-month low, public borrowing falls to a 9-year low

- ECB keeps key lending rates unchanged

Today’s Economic events

- Australia NAB quarterly business confidence 2 vs. 4 previously

- New Zealand Credit card spending y/y 4.10% vs. 6.0% previously

- Japan all industries activity m/m -1.0% vs. -1.0%

- Switzerland trade balance 3.55 billion vs. 3.49 billion

- UK retail sales m/m -0.90% vs. -0.40%

- UK public sector net borrowing 7.3 billion vs. 9.3 billion

- Canada wholesale sales m/m 1.80% vs. 0.20%

- ECB holds press conference

- Philly Fed manufacturing index -2.9 vs. 5.1

- US weekly unemployment claims 253k vs. 260k

Coming Up

- US house price index

- US existing home sales

- US CB leading index

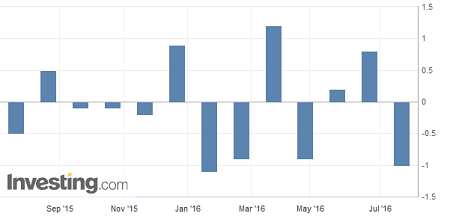

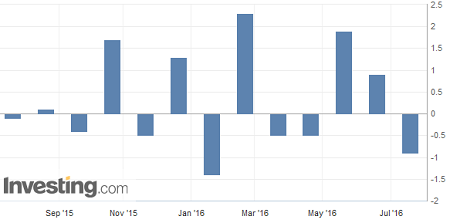

Japan all industry activity falls in May

The all industry activity index fell 1.0% on a month over month basis in May, falling for the first time in three months, data from the Japan’s ministry of economy, trade and industry showed on Thursday. The declines in May reversed the 0.80% increase seen in April, which was the first major increase in three months. Pushing the declines was growth in the construction activity which slowed to 1.50% from 2.0% previously while industrial production also fell 2.60% in May, following a 0.50% increase in April. On a year over year basis, the all industry activity rose 0.50% in May, compared to 0.20% declines in April.

The tertiary industry activity fell 0.70%, reversing the 0.70% increase seen in April.

The yen was however unaffected by the data with investors focusing on next week’s BoJ meeting. According to some media reports, BoJ officials are expected to expand the monetary base by a further 20 trillion yen, which was higher than the 10 trillion yen expansion, which was currently priced in. USDJPY touched a 6-week high, rising to 107.49 before easing back by the European trading session.

UK retail sales posts biggest fall in 6-month

Retail sales in the UK posted the sharpest monthly decline in nearly six months in June, data from the Office for National Statistics showed on Thursday. The slump in retail sales came on poor weather hurting clothing sales, while the impact on the Brexit vote was muted. The retail sales data was in sharp contrast to the recently released inflation report which surged mostly on higher airfares and the 2016 Euro Cup. Department stores managed to get a boost from consumer spending with sales coinciding with the Euro cup and the Queen’s birthday.

Retail sales fell 0.90% by sales volume, more than the expected declines of 0.90% that was forecast. Compared to a year ago, retail sales rose at a slower pace of 4.30% in June, down from 5.70% increase in May and fell more than the forecast of a dip to 5.0%.

Food sales were down 1.20% while non-food sales fell 0.80%. Department store sales fell 1.60% while clothing and footwear fell 1.80%. The ONS said that the survey was conducted between May 29 and July 2, noting that some of the responses were received in the week after the June 23 referendum vote.

Following the retail sales report, the UK’s public borrowing data also released showed that government borrowing fell to 7.8 billion pounds in June, compared to 10 billion a year ago. For the three months to June, public borrowing was 8.30% lower compared to a year ago.

US jobless claims continue to fall

The number of Americans filing for unemployment benefits last week fell, indicating a continued expansion into the second half of the year. Initial jobless claims, considered a proxy for layoffs in the US rose 253k in the week ending July 16, data from the US labor department showed on Thursday. This was lower than estimates of 260k. The latest data underlines the broad strength of hiring in the US labor markets with jobless claims seen to be steadily falling since spring of 2009. Fed Members continue to reiterate that there was more slack in the economy noting that the US had more opportunities to create jobs. The recent rebound in the US labor markets is likely to be seen as a positive for the US dollar as the Federal Reserve is expected to meet next week on July 26 – 27.

The US dollar maintained strong gains, posting a 4-month high with the US dollar index touching 97.36 yesterday before easing back lower. The broadly positive economic data from the US has rekindled expectations that the Fed is well suited to hike rates by September at the earliest. Later today, the US existing home sales report will be released with forecasts of a 0.90% decline in June on a month over month basis. Earlier this week, other data from the US housing markets included building permits which jumped 1.50% in June while housing starts rose 4.80%

ECB in a “wait and see” mode

The European Central bank, at its monetary policy meeting today left the key lending rates unchanged as widely expected. In the monetary policy statement, ECB President Mario Draghi said that despite the risks due to Brexit, the central bank would wait for more economic data before deciding on cutting interest rates further. The benchmark lending rate in the eurozone was unchanged at 0.0% while the deposit rate was steady at -0.40% and the marginal lending facility rate at 0.25%, unchanged. The euro was little changed on the news as investors shifted focus to the press conference by Mario Draghi which is currently under way.

So far, Draghi said that the financing conditions in the eurozone remain highly supportive and that the central bank would be in a better position to reassess its policies over the coming months. He said that if warranted, the central bank will act using all available instruments. On growth, Draghi said that domestic demand was supporting growth but said that the pace of growth in the second quarter was likely to be slower than that in Q1 with risks to the growth outlook tilted to the downside.