Note how the US dollar rebounded following the sell-off that was caused by last week’s Federal Reserve announcement. The recent rise in the US currency against the euro and other currencies has been mainly attributed to end-of-year borrowing of US dollars by non-US financial institutions and banks. Their main aim has been shoring up their accounts for regulatory purposes. These are known as cross currency swaps. We take a look at these financial flows and whether they are likely to last beyond the usual 2-3 weeks.

What are cross currency swaps?

A cross-currency basis swap is a contract whereby two parties borrow/lend from/to each other an equivalent amount of money denominated in two different currencies for a predefined period of time. For example, party A would borrows EUR 100 mln from party B in return for USD 117 mln.

The interest rate payments made during the swap are usually made on a quarterly basis and are determined off the interbank market, such as LIBOR (London Interbank Overnight Rate).

At the end of the swap, the nominal amounts are repaid at face value, which means the sums are not impacted by foreign exchange rate.

What is the ‘basis’ in cross-currency basis swaps?

Basis reflects the theory of interest rate parity shaping foreign exchange rates and interest rates. Interest rate parity theory states that the interest rate differential between holding two currencies over a stated of period of time, is covered by the difference between the spot and forward exchange rates over that same period of time.

When the theory stops working.

Does covered interest rate parity always works? No. And when it doesn’t, that’s where the “basis” comes in. An example: if EURUSD forward exchange rate is 2.10% above the spot rate, and the differential between US and Euro interest rates is 2.95 percentage points, the difference is minus 84 basis points. In this case, the basis of -84 points represents the difference between the spot and forward exchange rates that is not covered by the interest rate differential between the two currencies. In this example of negative EURUSD basis, the European entity seeking to borrow in USD pays a premium of 84 basis points as a cost of USD demand.

Who needs cross currency swaps?

A European bank or company in need of US dollar liquidity at year-end may find it difficult in terms of costs and regulatory requirements to take out a USD loan from a US bank. Therefore, the European entity is more likely to use its contacts in Europe to borrow in euros before exchanging these into dollars with another entity that needs euros.

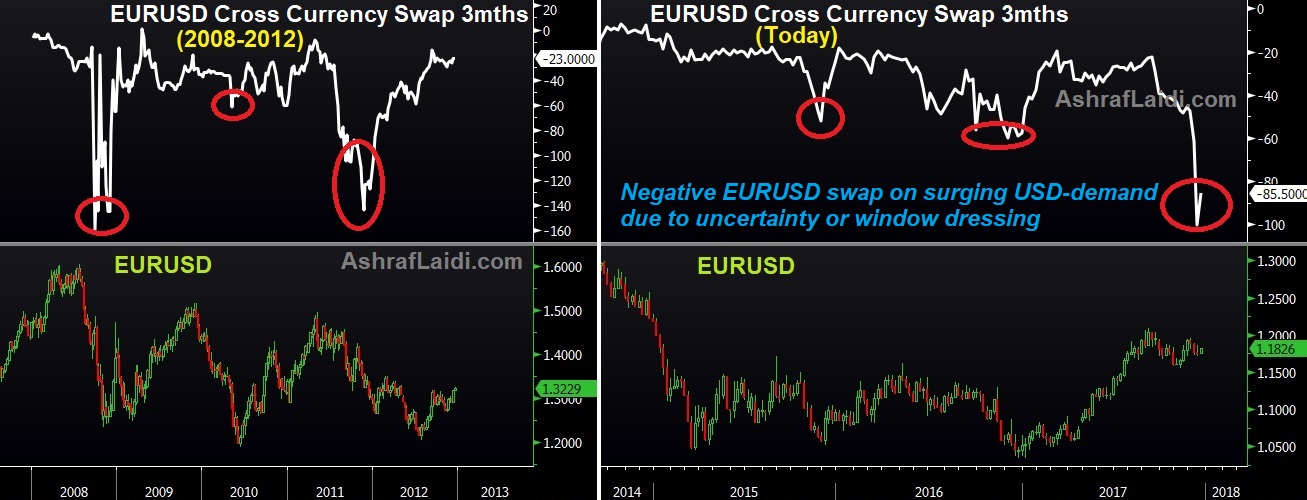

Why is the negative basis occurring now in EURUSD?

Cross currency basis borrowing generally occurs when demand for a certain currency emerges during economic or financial shocks. Surging demand for US dollars during the 2008 housing crisis and 2010 Eurozone crisis. But in the case of today, GDP growth in the Eurozone is at its strongest levels in over 5 years, banks are healthier and market volatility is low. The negative basis seen today in EURUSD is mainly a result of European entities rebalancing their deposits/reserves in order to either avoid the risk of holding excess of euros, or to hold more US dollars so as to meet regulatory requirements such as the upcoming MIFID II (Markets in Financial Instruments Directive part 2).

How long will it last?

In today’s circumstances, the reasons to the negative basis in EURUSD are nothing more than shifting flows, rather than major fundamental developments related to the US, Eurozone or their respective central banks. Whether this process dissipates in late December or January, I stick with my forecast for EURUSD to find support $1.1680 before interest re-emerges forces it towards $1.23 early next quarter.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)