The first trading month of the year is now history as traders shift focus to a busy week. Among the central bank meetings, the FOMC and the BoE meetings are likely to overshadow the Bank of Japan’s meeting this week. Still, no changes to monetary policy are expected this week from either of the central banks. In the UK, the Brexit bill is likely to top the agenda and could keep the British pound volatile. The week concludes with heavy data from the U.S. culminating with the January jobs report. China is closed for the first part of the week, celebrating the Chinese New Year. Here’s a quick guide to the currency markets for the week ending February 3rd, 2017.

FOMC to keep rates steady

The Federal Reserve will be meeting this week for the first monetary policy of the year. With no press conference scheduled for this week’s meeting, the expectation for a rate hike is low which would see the Fed funds rate remain unchanged at 0.75% after the Fed hiked rates by 25 basis points in December.

Assessing the economic data since the December rate hike, the U.S. economy has been posting steady gains especially with headline consumer inflation up 2.1%. The positive streak of data has led many officials to hold the view that the markets can expect at least two to three rate hikes this year. Friday’s consumer sentiment survey from the University of Michigan showed that data continues to point to inflationary pressures. Expectations on inflation, one year ahead rose to 2.6% in January, up from 2.2% in December, according to the UoM inflation expectations data released on Friday. The data suggests the likelihood that inflation could surge past the Fed’s forecasts which expect inflation to hit 2% in the next year or so.

The next major Fed meeting is in March, and depending on how the U.S. data turns out by then, the Fed could very well prepare the markets this week for another rate hike in March.

Eurozone GDP and inflation estimates

In the eurozone, the focus will turn to the GDP figures from the fourth quarter with economists expecting to see a 0.4% quarterly pace of growth in the three months ending December 2016. This would mark a modest uptick in growth, from 0.3% that was seen in the previous quarters. The yearly GDP growth rate for the Eurozone is expected to rise 1.7%, slightly down from a revised 1.8% as of the third quarter. Regional GDP releases over the week include numbers from France and Spain.

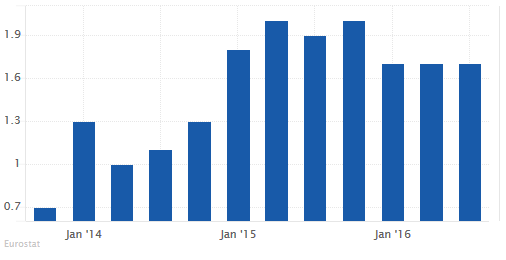

The Eurostat will also be releasing the flash inflation estimates for January on Tuesday. Economists are expecting to see the Eurozone headline inflation to rise 1.5% in January, up from an impressive 1.1% rise registered in December. However, the focus will be on the core inflation estimate which disappointingly is forecast to rise 0.9%, the same pace as the month before. A stubborn core inflation print will likely give the ECB officials enough reasons to maintain the QE which has come under pressure from Germany in recent months.

Bank of England to meet as UK parliament debates Brexit

The Bank of England’s monetary policy meeting due this week on February 2 comes at an interesting time when the UK’s Parliament will be in the midst of debating the Article 50 bill that will be introduced to the parliament on Tuesday. Economic data from the UK showed that consumers remained resilient despite the risks of Brexit. Latest GDP figures released on Friday showed that the UK’s economy expanded at a pace of 0.6% in the fourth quarter of 2016, rising at the same pace as in the third quarter. Inflation has also shot up following the plunge in the British pound, but manufacturing remains robust.

The Bank of England is expected to hold interest rates and asset purchases steady at this month’s meeting as it publishes new forecasts. Economists are geared up to see upgraded forecasts from the BoE both in terms of GDP growth and inflation. The BoE has so far maintained a view that the balance of risks remains equal while cautioning that the central bank will tolerate some overshoot of inflation.

The markets are currently turning hawkish on the BoE as they expect the central bank to signal a rate hike sooner than later but definitely not before March when the self-imposed deadline by PM May will see the Article 50 being triggered if it is approved by the parliament.