Image via World Economic Forum

- Will investors cheer or boo the BoJ’s policy decisions this week?

- Fed rate hike is down to the wire

- RBNZ remains overshadowed by BoJ and Fed

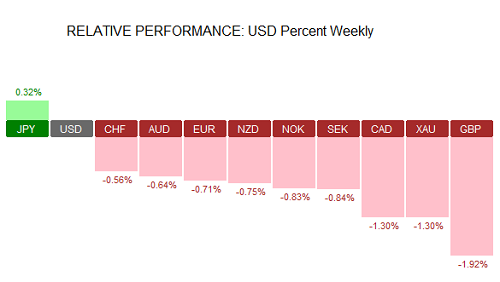

The Japanese yen managed to come out with some gains last week, only next to the US dollar. Despite a soft start to the week with weaker than expected economic releases, the US dollar managed to hold ground and got a boost after Friday’s inflation figures ascertained the dollar’s position. The Swiss franc was also better off compared to its peers, despite losing 0.56% for the week.

On the weaker end, the British pound continued to weaken from last week, with the declines seen accelerating. GBP lost over 1.92% by Friday’s close and was the weakest following the Canadian dollar which was down 1.30% on the week. Gold prices also closed bearish, losing 1.30% on the week.

Economic Calendar for the Week 19/09 – 23/09

| Date | Time | Currency | Event | Forecast | Previous |

| 20-Sep | 2:30 | AUD | Monetary Policy Meeting Minutes | ||

| AUD | HPI q/q | 3.10% | -0.20% | ||

| 13:30 | USD | Building Permits | 1.17M | 1.14M | |

| USD | Housing Starts | 1.19M | 1.21M | ||

| 17:45 | CAD | BOC Gov Poloz Speaks | |||

| 21-Sep | 01:30 | AUD | Mid-Year Economic and Fiscal Outlook | ||

| Tentative | JPY | Monetary Policy Statement | |||

| Tentative | JPY | BOJ Press Conference | |||

| 09:30 | GBP | Public Sector Net Borrowing | 10.5B | -1.5B | |

| 13:30 | CAD | Wholesale Sales m/m | 0.30% | 0.70% | |

| 19:00 | USD | FOMC Economic Projections | |||

| USD | FOMC Statement | ||||

| USD | Federal Funds Rate | <0.50% | <0.50% | ||

| 19:30 | USD | FOMC Press Conference | |||

| 22:00 | NZD | Official Cash Rate | 2.00% | 2.00% | |

| NZD | RBNZ Rate Statement | ||||

| 22-Sep | 13:30 | USD | Unemployment Claims | 261K | 260K |

| 14:00 | EUR | ECB President Draghi Speaks | |||

| 14:30 | GBP | MPC Member Cunliffe Speaks | |||

| 15:00 | USD | Existing Home Sales | 5.45M | 5.39M | |

| 23-Sep | 08:00 | EUR | French Flash Manufacturing PMI | 48.4 | 48.3 |

| EUR | French Flash Services PMI | 52 | 52.3 | ||

| 08:30 | EUR | German Flash Manufacturing PMI | 53.2 | 53.6 | |

| EUR | German Flash Services PMI | 52.2 | 51.7 | ||

| 09:00 | EUR | Flash Manufacturing PMI | 51.5 | 51.7 | |

| EUR | Flash Services PMI | 52.8 | 52.8 | ||

| 13:30 | CAD | Core CPI m/m | 0.20% | 0.00% | |

| CAD | Core Retail Sales m/m | 0.50% | -0.80% | ||

| CAD | CPI m/m | 0.10% | -0.20% | ||

| CAD | Retail Sales m/m | 0.20% | -0.10% |

Time: GMT+1

Currencies/Events to Watch this Week

AUD: A rather slow week for the Australian dollar, the only releases worth notice this week includes Tuesday’s monetary policy meeting minutes. The RBA held rates steady at its previous meeting but signaled that it was open to further rate cuts. Dovish meeting minutes could potentially put more pressure on the Australian dollar. Later, the mid-year economic and fiscal outlook report will also be coming out, although it is unlikely to be much of a market catalyst.

NZD: The RBNZ’s monetary policy meeting is also due on Wednesday, but consensus estimates point to no rate cuts at this meeting which could see the OCR unchanged at 2.0%. With broadly positive economic data coming out since the RBNZ’s last meeting and given the fact that there has been little in terms of inflation data to account for, the central bank could remain on the sidelines.

EUR: The Eurozone takes a backseat this week with a focus on Japan and the US. Still economic indicators this week is likely to shed light with flash PMI’s expected later in the week. The flash readings are likely to confirm the view that economic growth continues in the Eurozone at a moderate pace. No broad changes are expected for the September flash PMI’s but manufacturing could turn weaker if the current trend continues. The ECB will also be announcing the details of its TLTRO-II auction this week on Thursday.

GBP: The UK markets are also fairly quiet with no major releases following a busy economic week previously. BoE MPC Member Jon Cunliffe is expected to speak at a panel discussion on Thursday. His comments, if any references are made to monetary policy will be closely watched after last week’s BoE statement showed that the central bank is keeping the door open for another rate cut due following the November assessment. Still, it is a bit too early at this point in time. Besides the speech, UK’s public sector net borrowing data is expected on Wednesday along with the BoE’s quarterly economic bulletin.

JPY: The Bank of Japan’s meeting on Wednesday, September 21 will be one to watch out for potential policy changes. In July, the BoJ said that it would publish an assessment of its current monetary policy with changes likely to accompany, depending on the results of the assessment. The BoJ is expected to take the interest rates deeper into negative with the likelihood of delivering another 10 or 20bps rate cuts to the current -0.10%. There is also scope for additional easing from the BoJ as failure to come out strongly could potentially undermine the credibility of the Bank of Japan.

USD: While last week’s CPI data might have given some cheer for Fed hawks, the FOMC policy statement is likely to go down to the wire. The recent comments from Fed member showed a clear division between the hawks and the doves, but so far, the Hawks have managed to be the majority. While the market consensus expects the Fed to keep the Fed funds rate unchanged at 0.50%, there is potential for surprise. Still, in the event of the Fed keeping rates steady, the focus will be on the language in the policy statement the following press conference by Janet Yellen. Keeping rates unchanged at this week’s meeting could potentially push rate hike expectations to December.