Image via Federal Reserve

The Federal Reserve monetary policy meeting is due tomorrow. The Fed is expected to hold the fed funds rate steady at 0.25% – 0.50%, with traders gearing up to the FOMC statement, which could set the path for the forward guidance. The Fed’s next meeting after tomorrow is due only in September and could potentially pave the way for a possible rate hike then.

Brexit – Not as bad as it was thought to be

With the Brexit risks now a thing of the past, the equity markets have been broadly positive since then, largely due to hopes for more monetary policy stimulus from the BoJ, ECB and the Bank of England.

Alongside a softer Chinese yuan and receding risks in the international markets and a potentially upbeat domestic data, the Fed could keep the options for a September rate hike on the table. The futures markets, however, maintain the view that the Fed could hike rates only in December, but the odds could be seen improving as more data from the second quarter comes through.

Upbeat domestic data

The broad economic data from the US has been positive, but at its last meeting, the Fed was seen as being dovish following the May’s disappointing jobs report. While not much of economic data since then has been released and largely limited to the housing sector, the Fed is likely to keep its tone unchanged while assessing for more information, but the tone of the statement could tilt towards being hawkish.

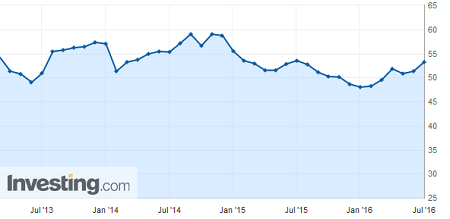

On the domestic data, early indicators show a turnaround in economic growth. The ISM manufacturing index rose to 53.2 in June, up from 51.3 in May, while the services index jumped to 56.5 in June, compared to 52.9 in May. The June payrolls report was also better than expected, rising 287k on the month while the weekly unemployment claims continue to run below the 300k average, consistent with the labor market data.

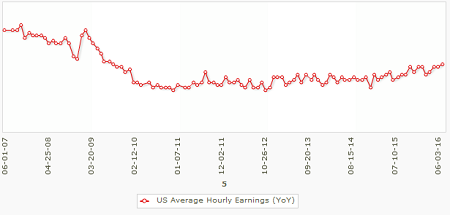

Wages were also seen growing with the average hourly earnings up 2.60% in June compared to a year ago, while core retail sales remain 4.30% higher for the same period.

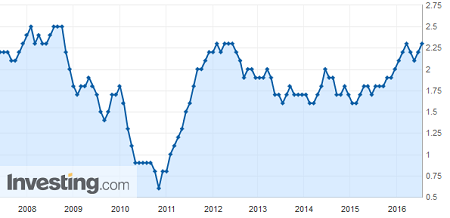

Core consumer prices also continue to strengthen, rising 2.30%. Recent PPI data also suggests that the underlying inflation continues to keep the view supported that consumer prices are likely to maintain their upward momentum.

The pickup in wages and consumer spending has also seen the US housing markets continue to rise steadily. Single-family housing starts edged higher, rising 13.40% compared to a year ago while price gains and low inventory for both new and existing home sales signal increasing demand in the sector. The Fed is, therefore, likely to upgrade its view of the economy and thus bring back rate hike expectations from December to September.

If the Fed’s statement does not change much from its June outlook, the chances are that the markets will focus on the meeting minutes which will be released on August 17, which could offer more insights and potentially show a hawkish narrative.

The US dollar index, which hit a 4-month high and started to pull back remains biased to the upside. As noted in last week’s commentary, the technical outlook for the dollar points to a near-term correction, potentially near 96 – 95 region, which could see the bullish trend resuming.