Image via RBNZ Museum

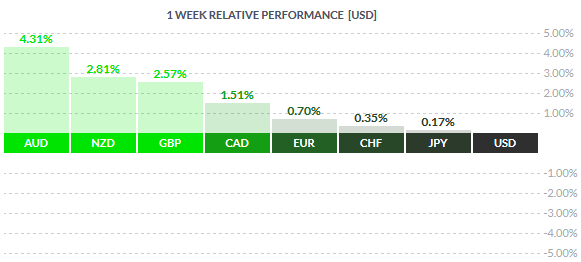

The US Dollar closed the week as the weakest currency as a strong risk-on sentiment saw the AUD and the NZD close the week with gains of 4.31% and 2.81% respectively. The gains came on a broadly positive data from Australia where last week the RBA left rates unchanged while the quarterly GDP expanded 0.60%, better than expected. The US Dollar, on the other hand, was weaker with the Nonfarm payrolls showing a decline in average wage earnings despite the unemployment rate staying at 4.90% for the second month in a row. The monthly number of jobs added to the economy also increased by 242k, beating estimates of 195k.

The British Pound was the surprise last week as the GBP closed with gains of 2.57%, just a week after GBPUSD fell to multi-year lows. The gains came despite a weaker than expected services PMI data and soft manufacturing and construction PMI survey data.

Fundamentals for the Week 07/03 – 11/03

| Date | Time | Currency | Detail | Forecast | Previous |

| 07-Mar | 00:30 | AUD | AIG Construction Index | 46.3 | |

| 02:30 | AUD | ANZ Job Advertisements m/m | 1.00% | ||

| 05:40 | JPY | BOJ Gov Kuroda Speaks | |||

| 07:00 | JPY | Leading Indicators | 101.60% | 102.10% | |

| 09:00 | EUR | German Factory Orders m/m | -0.40% | -0.70% | |

| 10:00 | CHF | Foreign Currency Reserves | 575B | ||

| 11:30 | EUR | Sentix Investor Confidence | 8.8 | 6 | |

| All Day | EUR | Eurogroup Meetings | |||

| 17:00 | USD | Labor Market Conditions Index m/m | 0.4 | ||

| 19:00 | USD | FOMC Member Brainard Speaks | |||

| 19:30 | USD | FOMC Member Fischer Speaks | |||

| 22:00 | USD | Consumer Credit m/m | 16.8B | 21.3B | |

| 23:45 | NZD | Manufacturing Sales q/q | 4.20% | ||

| 08-Mar | 01:20 | AUD | RBA Deputy Gov Lowe Speaks | ||

| 01:50 | JPY | Current Account | 1.66T | 1.64T | |

| JPY | Final GDP q/q | -0.40% | -0.40% | ||

| JPY | Bank Lending y/y | 2.30% | |||

| JPY | Final GDP Price Index y/y | 1.50% | 1.50% | ||

| 02:01 | GBP | BRC Retail Sales Monitor y/y | 2.60% | ||

| 02:30 | AUD | NAB Business Confidence | 2 | ||

| Tentative | CNY | Trade Balance | 329B | 406B | |

| 05:45 | JPY | 30-y Bond Auction | 1.07|3.0 | ||

| Tentative | CNY | USD-Denominated Trade Balance | 51.2B | 63.3B | |

| 07:00 | JPY | Consumer Confidence | 42.3 | 42.5 | |

| 08:00 | JPY | Economy Watchers Sentiment | 47.5 | 46.6 | |

| 08:45 | CHF | Unemployment Rate | 3.50% | 3.40% | |

| 09:00 | EUR | German Industrial Production m/m | 0.60% | -1.20% | |

| 09:45 | EUR | French Gov Budget Balance | -70.5B | ||

| EUR | French Trade Balance | -3.7B | -3.9B | ||

| 10:15 | CHF | CPI m/m | -0.10% | -0.40% | |

| 12:00 | EUR | Revised GDP q/q | 0.30% | 0.30% | |

| All Day | EUR | ECOFIN Meetings | |||

| 13:00 | USD | NFIB Small Business Index | 94.5 | 93.9 | |

| 15:15 | CAD | Housing Starts | 181K | 166K | |

| 15:30 | CAD | Building Permits m/m | 11.30% | ||

| 09-Mar | 01:30 | AUD | Westpac Consumer Sentiment | 4.20% | |

| 01:50 | JPY | M2 Money Stock y/y | 3.20% | 3.20% | |

| 02:30 | AUD | Home Loans m/m | -2.70% | 2.60% | |

| 08:00 | JPY | Prelim Machine Tool Orders y/y | -17.20% | ||

| 11:30 | GBP | Manufacturing Production m/m | 0.20% | -0.20% | |

| GBP | Industrial Production m/m | 0.60% | -1.10% | ||

| 17:00 | CAD | BOC Rate Statement | |||

| CAD | Overnight Rate | 0.50% | 0.50% | ||

| GBP | NIESR GDP Estimate | 0.40% | |||

| USD | Wholesale Inventories m/m | -0.20% | -0.10% | ||

| 17:30 | USD | Crude Oil Inventories | 10.4M | ||

| 22:00 | NZD | Official Cash Rate | 2.50% | 2.50% | |

| NZD | RBNZ Rate Statement | ||||

| NZD | RBNZ Monetary Policy Statement | ||||

| 22:05 | NZD | RBNZ Press Conference | |||

| 10-Mar | 01:50 | JPY | PPI y/y | -3.40% | -3.10% |

| 02:00 | AUD | MI Inflation Expectations | 3.60% | ||

| 02:01 | GBP | RICS House Price Balance | 52% | 49% | |

| 03:30 | CNY | CPI y/y | 1.80% | 1.80% | |

| CNY | PPI y/y | -4.90% | -5.30% | ||

| 08:30 | EUR | French Final Non-Farm Payrolls q/q | 0.20% | 0.20% | |

| 09:00 | EUR | German Trade Balance | 19.2B | 19.4B | |

| 09:45 | EUR | French Industrial Production m/m | 0.80% | -1.60% | |

| 11:00 | EUR | Italian Quarterly Unemployment Rate | 11.50% | 11.70% | |

| 14:45 | EUR | Minimum Bid Rate | 0.05% | 0.05% | |

| 15:30 | CAD | NHPI m/m | 0.20% | 0.10% | |

| CAD | Capacity Utilization Rate | 81.90% | 82.00% | ||

| EUR | ECB Press Conference | ||||

| USD | Unemployment Claims | 272K | 278K | ||

| 20:01 | USD | 30-y Bond Auction | 2.50|2.1 | ||

| 21:00 | USD | Federal Budget Balance | -198.3B | 55.2B | |

| 23:15 | CAD | BOC Gov Poloz Speaks | |||

| 23:30 | NZD | Business NZ Manufacturing Index | 57.9 | ||

| 23:45 | NZD | FPI m/m | 2.00% | ||

| 11-Mar | 01:50 | JPY | BSI Manufacturing Index | 4.2 | 3.8 |

| 09:00 | EUR | German Final CPI m/m | 0.40% | 0.40% | |

| 11:00 | EUR | Italian Industrial Production m/m | 0.90% | -0.70% | |

| 11:30 | GBP | Trade Balance | -10.3B | -9.9B | |

| GBP | Construction Output m/m | -1.30% | 1.50% | ||

| GBP | Consumer Inflation Expectations | 2.00% | |||

| 15:30 | CAD | Employment Change | 10.2K | -5.7K | |

| CAD | Unemployment Rate | 7.20% | 7.20% | ||

| USD | Import Prices m/m | -0.70% | -1.10% |

Time: GMT+2

Currencies/Events to Watch this Week

NZD: NZD: The Reserve Bank of New Zealand will be meeting this week on March 9th. Expectations are that the Central Bank would hold rates steady at 2.50%. This view comes as RBNZ Wheeler had reiterated that low inflation was likely to persist and more recently at a speech, he said that the bank would avoid taking a mechanistic approach to monetary policy. While it could be a close call, the RBNZ is more likely to watch for more economic data before cutting rates at its meeting this week.

JPY: JPY: The final revision to the fourth quarter GDP will be the main event for the Yen. Expectations are unchanged at -0.40%. Ahead of the GDP data, BoJ’s Kuroda is due to speak early on Monday which could be a key risk for the Yen. On Friday the BoJ Governor said that the Central Bank wasn’t considering cutting interest rates further at this point in time. The Yen had mildly strengthened on his comments as speculation eased that the BoJ could act in March. However, in his comments, Kuroda said that the Central bank would act if needed. The early comments on Monday are likely to see some volatility in the Yen ahead of the GDP data due for release, later on, Tuesday.

EUR: The ECB’s big meeting looms on March 10th which comes after the final revised quarterly GDP numbers due on Tuesday. Expectations are for the GDP to remain unchanged at 0.30% for the fourth quarter of 2015. The ECB’s meeting and press conference will be closely watching as Mario Draghi and team haven’t left any clear signals on what the central bank will decide. On Friday rumors floated that there was no consensus among the ECB members, except to cut deposit rates. While nothing has been confirmed yet, the uncertainty in the decision is likely to see a stronger impact on the Euro.

GBP: The week ahead for the GBP is quiet with the exception of manufacturing and industrial production. Estimates point to a possible recovery in manufacturing production and industrial production forecasted to rise 0.20% and 0.60% respectively, following sharp declines previously. The British Pound ignored a weak set of data last week and surged ahead just a week after posting strong losses. It is more likely that the British Pound will continue to focus on the Brexit issues than any economic releases for the time being.

CAD: The week ahead will see two main events affecting the Canadian dollar. First off, the Bank of Canada is expected to meet on 9th March. The BoC is expected to hold rates steady at 0.50% with Oil prices rebounding strongly and previous inflation numbers coming out modestly better than expected including the monthly GDP data which showed an increase of 0.20%. Following the BoC’s decision, Friday will see the release of the February Canadian jobs numbers. Canadian unemployment rate is expected to remain unchanged at 7.20% while the monthly jobs are expected to rise 10.2k for the month in February.

USD: Data from the US this week is soft with no major releases in sight. A few Fed members are expected to speak over the week which is the only key risk to the Greenback. Following Monday’s Fed speak, the remainder of the day will see the Fed blackout period as the Central bank is due to meet the week after, leaving the stage for the Euro and the ECB this coming week.