Following a rather volatile week, the markets will likely continue playing to the Trump election victory tune. However, as the news fades, the focus will now shift back, at least temporarily to the economic data. Inflation once again is the main theme this week with US, UK, Eurozone, and Canada due to the monthly inflation data while Fed Chair Janet Yellen and ECB President Mario Draghi’s speeches will be under the scanner.

Volatility is likely to continue this week

The markets fell then bounced back sharply but to think that it is a done deal and that all is well with the risk sentiment is being short sighted. The current volatility in the markets is perhaps a mere reflection of the uncertainty that is likely to continue. While president elect Trump’s speech offered some solace alongside other leaders pledging their support, the markets remain acutely tuned to any rhetoric from the next US president.

US Inflation Report

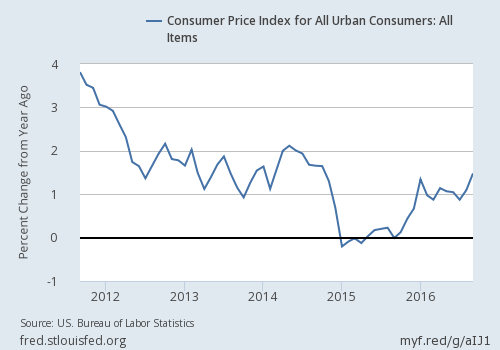

Next week, the US CPI report, due on Thursday will be of importance, coming at a time where the markets are doing the flip-flop on the prospects of a December rate hike. Initially after the election results, the markets remained doubtful of a Fed rate hike, but prospects picked up thereafter as over the week, Fed members such as Williams and Bullard drove home the point that the Fed rate hike narrative was still alive.

This week’s inflation figures will more likely cement the view. Headline inflation in the US jumped 0.3% in September, and the forecasts point to a 0.4% increase in October. This would bring the yearly inflation rate to 1.6% and if data comes out as expected, it would confirm the highest inflation rate since October of 2014. The basis for higher inflation comes on expectations of higher energy prices. Excluding the volatile components, core inflation is expected to rise 0.2% during October, slightly higher from 0.1% previously.

Besides inflation, retail sales numbers (expected: 0.6%) will be coming out earlier on Tuesday followed by industrial production (expected: 0.2%) data on Wednesday. Retail sales numbers are tipped to have increased in the month of October underlining a solid start to Q4.

Eurozone, inflation, and GDP numbers

A reasonably busy week from the eurozone will see more data from Germany. Last week’s industrial and manufacturing numbers came out weak leading many to conclude that German growth could be seen slowing.

Preliminary GDP estimates from Germany will be released on Tuesday and forecasts point to a 0.3% quarterly GDP growth in Q3, down from 0.4% previously. French and Italian GDP numbers will also be coming out followed by flash GDP estimates, which is expected to show no change as the GDP stands at 0.3% for the third quarter.

Inflation data from the eurozone on Thursday is expected to show a 0.4% year over year increase on the headline while core CPI is expected at 0.8% for the same period. The inflation data could see some re-pricing in the euro where expectations for the ECB’s QE tapering builds up into the December ECB meeting.

UK Inflation and Unemployment Report

The British pound enjoyed a strong rally during the election led volatility, but the focus will be back on the inflation and jobs report coming out this week. Headline inflation in the UK is expected to rise 1.1%, up from 1% increase seen in September, while core inflation is expected to rise at the moderate pace of 1.4% during the month.

The UK labor market data is due on Wednesday with estimates showing a 2.3% increase in average earnings index, rising at the same pace as before, while the unemployment rate is expected to hold at 4.9%.

On Thursday, UK’s retail sales figures are out with economists expecting a 0.5% increase in retail sales for October.