The markets enter a crucial week with both economic and political decisions weighing on traders. The US general election is now just one week away which will remain in the backdrop for the markets. The monetary policy meetings from the RBA, BoJ, FOMC and the Bank of England will likely set the stage for a December showdown. On the economic front, US nonfarm payrolls and ISM data, Eurozone GDP and inflation figures and the UK and China’s PMI numbers will be other economic releases of importance coming up over the week.

Central banks seen holding policy steady

There are four central bank meetings scheduled for the week ahead, and it is quite likely that all four central banks will be keeping their respective key interest rates on hold this week as the expectations of a Fed rate hike for December seems to be increasingly likely.

The RBA’s monetary policy is the first set the ball rolling on Tuesday, and rates are expected to remain put at 1.50%. Recent inflation figures, although not up to the mark was seen as a positive sign. Australia registered a quarterly inflation rate of 0.7% or 1.30% on a year over basis. It is still below the RBA’s target rate, but the new RBA Governor, Lowe signaled that rates would remain stable in the near term.

The Bank of Japan’s meeting comes up later in the day on Tuesday. After the BoJ’s new policy measures announced in September, economists do not expect to see any surprises coming out of the BoJ’s meeting this week. Although inflation remains a major concern with last week’s BoJ core inflation gauge slowing to 0.2% increase on a month over month basis.

The yen’s exchange rate is also likely to see the BoJ stand pat on a policy which has been relatively stable over the past few weeks. In all likelihood, the BoJ officials are likely to push any policy decisions, if any to the December meeting.

The FOMC meeting is up on Wednesday, and no changes to the Fed funds rate is expected in light of the US elections due just a week later. Still, the FOMC statement could likely give clues for a potential rate hike in December, which will be the second rate hike in almost a year. Some voting members are likely to dissent at this week’s meeting as well, voting for a rate hike instead of maintaining the status quo.

The Bank of England’s policy meeting will likely garner more attention. No changes to rates are expected in light of the recent surge in inflation and a better than expected economic performance in the third quarter.

The QE purchases could also be held steady which could give some support to the GBP to the upside. Forward guidance from the BoE will be crucial as the markets now price out further rate cuts from the central bank.

UK: October PMI’s and inflation report

Manufacturing, construction and services PMI from the UK for October will be in focus this week. Manufacturing and construction PMI’s were seen to be steadily rising for two consecutive months since August while services PMI was seen sliding from August highs of 52.9 to register a soft print of 52.6 in September. A broad pick up in the three sectors could reinforce expectations that the UK’s economy is likely to remain robust into the fourth quarter. A slowdown in the respective sectors could, on the other hand, spark further selling pressure on the GBP.

The BoE’s inflation report is also due this week. Although BoE Governor Mark Carney said that the central bank was likely to tolerate an overshoot of inflation and forecasts a 1.5% – 1.8% inflation by spring 2017, the inflation report could give clues from the BoE on how the central bank will likely steer its monetary policy amid rising inflation.

US nonfarm payrolls and ISM data

The ISM manufacturing PMI data due to be released this week on Tuesday is expected to show a steady print. Economists expect the October manufacturing PMI to rise to 51.8. This follows a September increase of 51.5 and could be seen as a positive for the Fed rate hike in December.

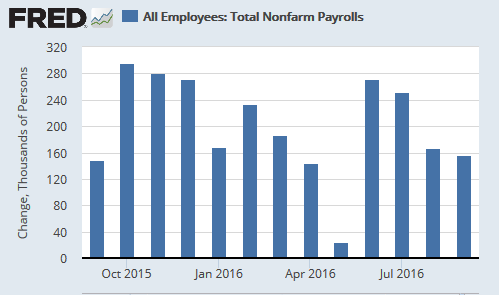

Friday’s payrolls report will be the second jobs report before the December FOMC meeting. After payrolls rose 156k in September, the market expectations are for a headline NFP print of 175k with the unemployment rate expected to slip back to 4.9% after unexpectedly rising to 5.0% in September. The average hourly earnings are also expected to rise 0.3% last month, a notch higher from 0.2% print registered in the previous month.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)