Following an uneventful week which saw the Bank of Canada and the European Central Bank maintaining the status quo, the pace of economic data is seen to be slowing in the coming week. While last week was all about inflation numbers, this week the focus shifts to GDP numbers coming out of the US, UK, and France.

US third quarter GDP growth

The US dollar will be looking to a relatively slow start to the week with most of the first half of the week seeing flash PMI data for the month of October. Following the turnaround in the PMI’s (both Markit and ISM), the preliminary data will give a view of the manufacturing and non-manufacturing sector performance. US durable goods numbers will be coming up on Thursday. After a 0.2% decline in core durable goods orders and a flat print on the headline for August, the numbers for October are forecast to rise 0.2% and 0.1% respectively.

The week is also marked by several Fed member speeches ahead of the October 25 blackout period in the run up to early November FOMC meeting. The markets are currently assigning a 20% probability of a rate hike at the November meeting.

Friday’s advance GDP report will be the main event risk for the US dollar and its peers. After a slow period of growth in Q1 and Q2, expectations are high with forecasts pointing to a 2.50% increase in growth. In the second quarter, US GDP registered a meager 1.40% GDP growth.

Australia quarterly inflation

Ahead of the RBA’s meeting in November, the third quarter inflation figures will be released this Wednesday. After a 0.40% increase in headline inflation during the second quarter, economists are expecting to see the third quarter inflation rise 0.5%. The trimmed mean CPI is expected to rise 0.4% during the quarter, following a 0.50% increase previously.

Last week, the new RBA Governor, Philip Lowe gave his first speech where he ruled out further rate cuts while expressing concerns that inflation could be well anchored to the downside. As long as the third quarter inflation does not surprise to the downside, the RBA is expected to keep interest rates on hold in the coming weeks.

UK Q3 preliminary GDP

With the British pound vulnerable to the politics and the Brexit narrative, the advance third quarter GDP numbers from the UK will be published by the ONS on Thursday. Forecasts point to a 0.3% increase in GDP during the quarter ending September. This, following a final revised Q2 GDP print of 0.70%. The third quarter GDP numbers will be the first after the UK voted to leave the EU in June. However, the data is unlikely to have much of an impact as the real deal comes after the UK has formally ended its relationship with the EU. As evidenced by the recent volatility in the GBP which has plunged below its Brexit lows, the data is unlikely to offer much.

BoE Governor Mark Carney will also be speaking during the week. His speech could come under the scanner ahead of the BoE’s next policy meeting in November. The central bank had previously communicated that it would conduct another assessment of the economy to determine if another rate cut was warranted. Latest inflation figures from the UK showed consumer prices rising steadily on the back of a weaker exchange rate, which puts to question whether the Bank of England will stoke inflation further by cutting interest rates. In this aspect, the central bank governor’s speech could offer clues into the next policy decisions from the BoE.

Draghi’s speech

The ECB president, Mario Draghi is expected to speak next week. After Draghi offered very little for the markets at the ECB policy meeting last week, the question that remains is whether the central bank will start tapering its QE after March 2017 or if the central bank will continue its bond purchase program beyond March. The euro fell sharply last week already in anticipation that the ECB could expand its QE beyond March.

While it is unlikely to expect Draghi to give away too much at this week’s speaking engagement references to euro area growth, inflation and monetary policy, in general, could be seen as a dovish signal from Draghi that could only build up expectations for another round of easing from the ECB.

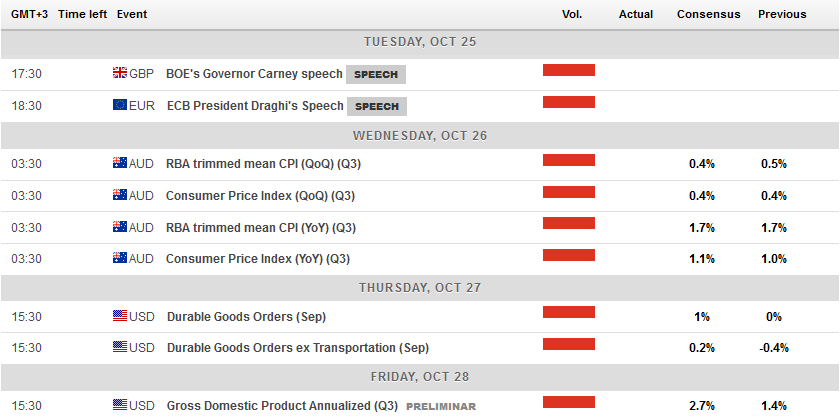

Economic Calendar: 24 – 28 Oct