After a rather busy week which saw new economic reports for the month of January, the markets will be slowing down this coming week with most of the data confined to second-tier from the US, UK, and Europe. Standing out from this will be the central bank decisions from the RBA and the RBNZ, both of which are expected to keep interest rates steady. A busy week for Mexico will see the central bank interest rate decision which comes after the inflation data on Thursday. In Europe, the focus will be on the Nordics where Norway will be releasing the inflation figures.

RBA policy decision: No changes expected

The Reserve Bank of Australia will be holding its monetary policy meeting this week, the first for this year. The Australian bond markets continued to slide most of the last week. Yields on the 10-year note which runs inversely to bond prices rose by over one basis point to 2.77%, and bond traders are likely to hold ahead of the RBA’s meeting on Tuesday.

The central bank is expected to keep the benchmark lending rates steady at 1.50% amid an uncertain outlook. In December, the meeting minutes showed that members were concerned on the need to balance the economic and financial risks while maintaining stability.

The economy continues to remain in transition with the unemployment rate staying flat for nearly nine months now and the most recent fourth quarter full-time employment alleviates the concern. However, in the near term, the central bank is expected to stand pat on policy.

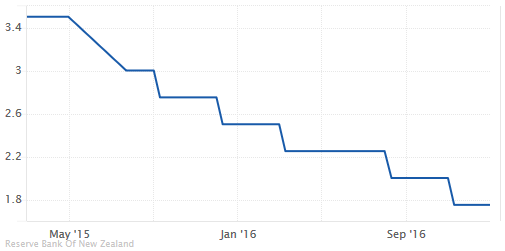

RBNZ expected to keep rates steady at 1.75%

The Reserve Bank of New Zealand will be meeting this week on February 9th, for its first monetary policy review this year. The central bank is expected to hold the OCR unchanged at 1.75%. The central bank’s meeting comes on the back of what could be the start of a recovery in inflation as New Zealand’s inflation rate was seen returning to the central bank’s target band for the first time in nearly two years.

There was also evidence of stronger inflationary pressures building as other measures of core inflation was also seen rising. So far, inflation expectations have remained stable with the most recent data showing a headline print of 1.7%. Further evidence of this comes earlier in the week on the 7th of February before the RBNZ’s meeting.

With the U.S. Federal Reserve expecting to hike rates three times this year, the inclination for easing from other central banks is also slowly waning. Fiscal expansion continues to remain at the forefront globally. While the RBNZ is expected to keep rates steady at this week’s meeting, the issue of a stronger exchange rate is also likely to be addressed as the Kiwi is around 4% higher from the RBNZ’s November projections.

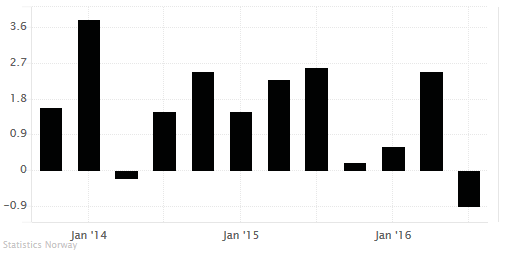

Norway GDP and CPI

A busy week from Norway, the week ahead will see key data including inflation and fourth quarter GDP numbers including manufacturing production.

GDP in Norway is expected to rise 0.4% on a quarterly basis in the fourth quarter, up from 0.2% in third quarter. The annual GDP growth rate showed a 0.9% contract in the third quarter. The Norges Bank has forecast a growth of around 0.3%. Growth is expected to brush aside the drag from the continued weakness in the oil sector boosted by growth from production, construction and services sectors.

Inflation figures are also coming out, and forecasts point to a 2.6% increase on a yearly basis in January. This would see a slight increase from 2.5% previously but would still put inflation below the Norges Bank forecast of 2.94%. Uncertainty on food prices continues to remain high after prices fell significantly in the month before.

![Credit Card 160×600 [EN]](https://assets.iorbex.com/blog/wp-content/uploads/2023/06/13144507/Blog-Banner_EN-Banner_160X600X2.webp)