The European Central Bank will be meeting this week on Thursday for its first monetary policy meeting for this year. It’s been a year since the ECB announced its QE program in January 2015 in a bid to stoke inflation. However, so far the ECB has had nothing to show with inflation staying weak.

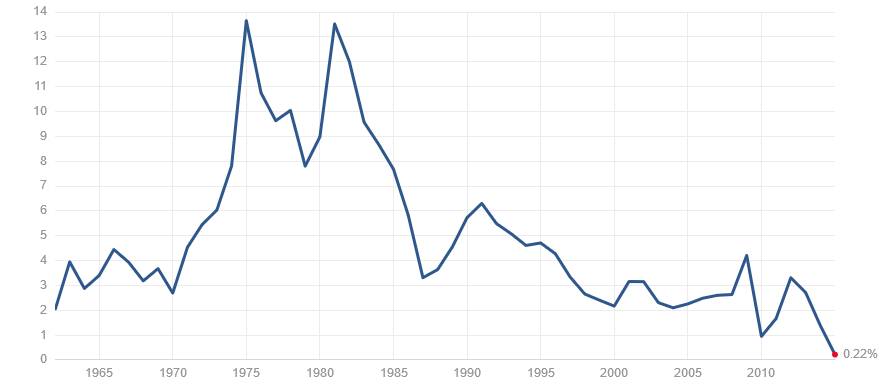

As the Eurozone inflation graph shows above, inflation has remained sharply subdued since 2010 staying consistently below the 2.0% target inflation rate. Slower industrial production and weak GDP which currently stands at 1.40%, alongside weak Oil prices have led to deflationary pressures despite the bond purchase program. The original timeline for the QE, when it was announced in January 2015 was to end by September 2016.

Coming off December’s policy decision where the Central Bank cut the deposit rates by 20bps, to -0.30% but fell short from expanding the €60 billion QE, not much is expected in terms of policy measures at this meeting after announcing to keep the bond purchases going beyond September 2016.

The ECB could instead look to this month’s meeting to assess the economic recovery and more importantly, inflation numbers in the Eurozone area. Indeed, a mere one month data is unlikely to make the ECB announce strong policy measures which open the debate to a potential policy decision being taken at the March ECB meeting.

[Tweet “EU: Inflation remained sharply subdued since 2010 staying consistently below the 2.0% target “]

During its December meeting, the ECB noted that it is most likely to miss the inflation forecasts for 2016 and 2017. Since December, Eurozone inflation has remained flat with the latest inflation data released earlier this week on 19th January confirming the Eurozone headline CPI rate at 0.20% and the Core CPI at 0.90% year on year.

By committing itself to more QE, the ECB could potentially open the way for further continued easing down the road and could potentially risk a Japan type of QE which shows no signs of abating. In light of the above, the ECB could potentially be looking at weakening the Euro, relative to the Dollar in hopes that the weaker exchange rate could help boost inflation while waiting for Oil prices to find a bottom.

The next couple of months is likely to see the Eurozone inflation continuing to remain flat if not weaken further on Oil prices, which potentially opens the debate for a bearish outlook on the EURUSD in the coming months. However, should Draghi signal for March’s ECB meeting to decide on further expansion, it is most likely to be big considering that the ECB’s credibility has been in question after failing to act in December last year. On the other side of the scale, the Federal Reserve will also need to be closely watched as further rate hikes could help keep the Euro subdued to the US Dollar, but Draghi will also need to watch out for policy decisions from China where we have seen time and again that a Yuan devaluation has helped prop up the single currency.

[Tweet “ECB is no doubt walking a thin line, with weak Oil prices, Fed’s rate hikes and Yuan devaluation”]

Considering all the above variables, the ECB is no doubt walking a thin line, with weak Oil prices, Fed’s rate hikes and Yuan devaluation all playing a major role not just on inflation but also on the exchange rates. At today’s ECB meeting, we can expect to see some dovish talk from Draghi while the question remains if the ECB will or will not signal further QE easing in March 2015, which if announced, this time, around will need to see Draghi follow through with his promises unlike in December last year.

#Vote: Do you think #ECB will extend its #QE program?

— Orbex (@OrbexFX) January 21, 2016