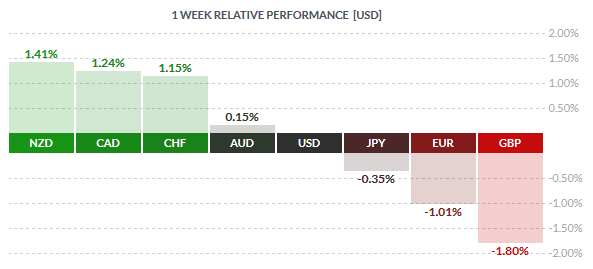

The Kiwi and the Canadian dollar emerged at the top last week gaining 1.41% and 1.24% respectively. The gains came as the RBNZ left interest rates unchanged at its meeting last week, sending the NZDUSD to post new yearly highs. The Canadian dollar which was fairly muted for the most of the week surged on Friday after the monthly jobs report saw the Canadian unemployment rate falling to 6.90% and beating forecasts by a strong margin.

At the tail end, the British pound was the weakest, losing 1.80% against the US dollar. The sterling was volatile for the most part of the week, in fact, gapping lower on Monday on new opinion polls. While the currency managed to gain back the losses, on Friday another set of opinion polls, in favor of the ‘Leave’ camp sent the pound weaker. The euro, which was flat for the most of the week started to decline after briefly trading near $1.14 earlier in the week.

Fundamentals for the Week 13/06 – 17/06

| Date | Time | Currency | Event | Forecast | Previous |

| 13-Jun | 3:00 | CNY | Industrial Production y/y | 6.10% | 6.00% |

| 14-Jun | 09:30 | GBP | CPI y/y | 0.40% | 0.30% |

| 13:30 | USD | Core Retail Sales m/m | 0.40% | 0.80% | |

| USD | Retail Sales m/m | 0.40% | 1.30% | ||

| 15-Jun | 09:30 | GBP | Average Earnings Index 3m/y | 1.70% | 2.00% |

| GBP | Claimant Count Change | 0.1K | -2.4K | ||

| 13:30 | CAD | Manufacturing Sales m/m | -0.90% | ||

| USD | PPI m/m | 0.30% | 0.20% | ||

| Tentative | NZD | GDT Price Index | 3.40% | ||

| 19:00 | USD | FOMC Economic Projections | |||

| USD | FOMC Statement | ||||

| USD | Federal Funds Rate | <0.50% | <0.50% | ||

| 19:30 | USD | FOMC Press Conference | |||

| 23:45 | NZD | GDP q/q | 0.50% | 0.90% | |

| 16-Jun | 00:55 | CAD | BOC Gov Poloz Speaks | ||

| 02:30 | AUD | Employment Change | 15.1K | 10.8K | |

| AUD | Unemployment Rate | 5.70% | 5.70% | ||

| Tentative | JPY | Monetary Policy Statement | |||

| Tentative | JPY | BOJ Press Conference | |||

| 08:30 | CHF | Libor Rate | -0.75% | -0.75% | |

| CHF | SNB Monetary Policy Assessment | ||||

| CHF | SNB Press Conference | ||||

| 09:30 | GBP | Retail Sales m/m | 0.20% | 1.30% | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0-0-9 | 0-0-9 | |

| GBP | Monetary Policy Summary | ||||

| GBP | Official Bank Rate | 0.50% | 0.50% | ||

| 13:30 | USD | CPI m/m | 0.30% | 0.40% | |

| USD | Core CPI m/m | 0.20% | 0.20% | ||

| USD | Philly Fed Manufacturing Index | 1.1 | -1.8 | ||

| USD | Unemployment Claims | 267K | 264K | ||

| 17-Jun | 13:30 | CAD | Core CPI m/m | 0.20% | |

| USD | Building Permits | 1.15M | 1.12M | ||

| 16:00 | EUR | ECB President Draghi Speaks |

Time: GMT+1

Currencies/Events to Watch this Week

AUD: The Australian markets look to a short trading week with Monday closed on account of ‘Queen’s Birthday’. Later in the week, the monthly jobs report for May is expected to show the unemployment rate holding steady at 5.70%. This would be a steady print in the number for the third consecutive month. The Australia economy is expected to show 16k jobs being added on the month; this is slightly higher from April’s 10.8k

NZD: Following last week’s no change to interest rates from the RBNZ, the week ahead will focus on the current account data from New Zealand for the first quarter. The current account to GDP is expected to show continued declines with forecasts pointing to a -2.90% print; this is moderately slower than the previous quarter’s 3.10% declines. Later on Wednesday, the quarterly GDP report is expected to show that the New Zealand economy expanded at a slower pace of 0.60% in the first three months of the year. This is slower than the fourth quarter’s 0.90% increase. On an annualized basis, GDP is expected to rise modestly higher to 2.40% from 2.30% previously.

JPY: The focus this week will be the Bank of Japan’s meeting on Thursday, June 16th. Expectations are broadly divided, but the case for a surprise rate cut looms. The BoJ, according to some estimates could cut interest rates by 10 or 20 basis points at this week’s meeting. On the other hand, economists argue that with monetary policy failing to do much and in the backdrop of the delay in sales tax hike, the BoJ could sit on its hands and this week’s meeting. Besides the BoJ, industrial production numbers are due on Tuesday.

GBP: Monthly inflation data from the UK comes out on Tuesday. The core CPI is expected to rise 1.20% on the month, rising at the same pace as in April. The headline CPI, on the other hand, is expected to rise 0.40% in May, extending the 0.30% increase from April. PPI data is also due on the same day. On Wednesday, UK’s monthly labor report is expected to show that the unemployment rate continues to hold at 5.10%. But average earnings with bonuses are expected to rise at a slower pace of only 1.60% on the month in April, down from 2.0% in the previous month. Excluding bonuses, average hourly earnings are expected to rise 2.0% compared to 2.10% previously. Retail sales numbers are due on Thursday and expected to show a moderation following March’s strong increase. Later in the day, Bank of England’s monetary policy meeting is expected to show no change.

CHF: Data from Switzerland is limited to the PPI data on Tuesday, but the focus turns to the SNB’s meeting on Thursday, June 16th. The SNB’s Libor rate is expected to remain unchanged at -0.75%

EUR: Data from the Eurozone is relatively light in comparison to its peers. Industrial production numbers are up on Tuesday and expected to show a month over month increase of 0.40% and 10% year over year increase, this is a strong forecast, after industrial production fell 0.80% in March and increased only 0.20% on a year over year basis. French and Eurozone monthly inflation numbers for May is lined up during the week.

CAD: From Canada, economic data is light with manufacturing sales coming out Wednesday. On Friday, the monthly inflation numbers for May is expected to show a headline month over month increase of 0.50% compared to 0.30% increase in April. On a yearly basis, Canada’s consumer inflation is expected rise at the same pace of 1.70% from the previous month.

USD: A busy and an important week for the US dollar. On Tuesday retail sales numbers are up and expected to moderate. The headline print is expected to show that retail sales increased 0.40% in May, easing back from the 1.30% surge in April, while core retail sales excluding auto are expected to rise 0.40%, down from 0.80% a month ago. PPI data is due out on Wednesday followed by industrial production numbers. But the focus on the day will be the FOMC meeting. Staff economic projections will be released, and Janet Yellen will be holding a press conference later. The Fed funds rate is expected to remain unchanged at 0.50%. The remainder of the week is filled with monthly inflation figures which are expected to show no big surprises, followed building permits and housing starts data.